China Carbon Market (2025-2031) | Trends, Industry, Analysis, Outlook, Size, Companies, Revenue, Forecast, Value, Growth & Share

Market Forecast By Product Types (Amorphous Carbon, Graphite, Diamond), By Applications (Automotive, Construction, Engineering Industries, Aerospace, Others) And Competitive Landscape

| Product Code: ETC004118 | Publication Date: Sep 2020 | Updated Date: Oct 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

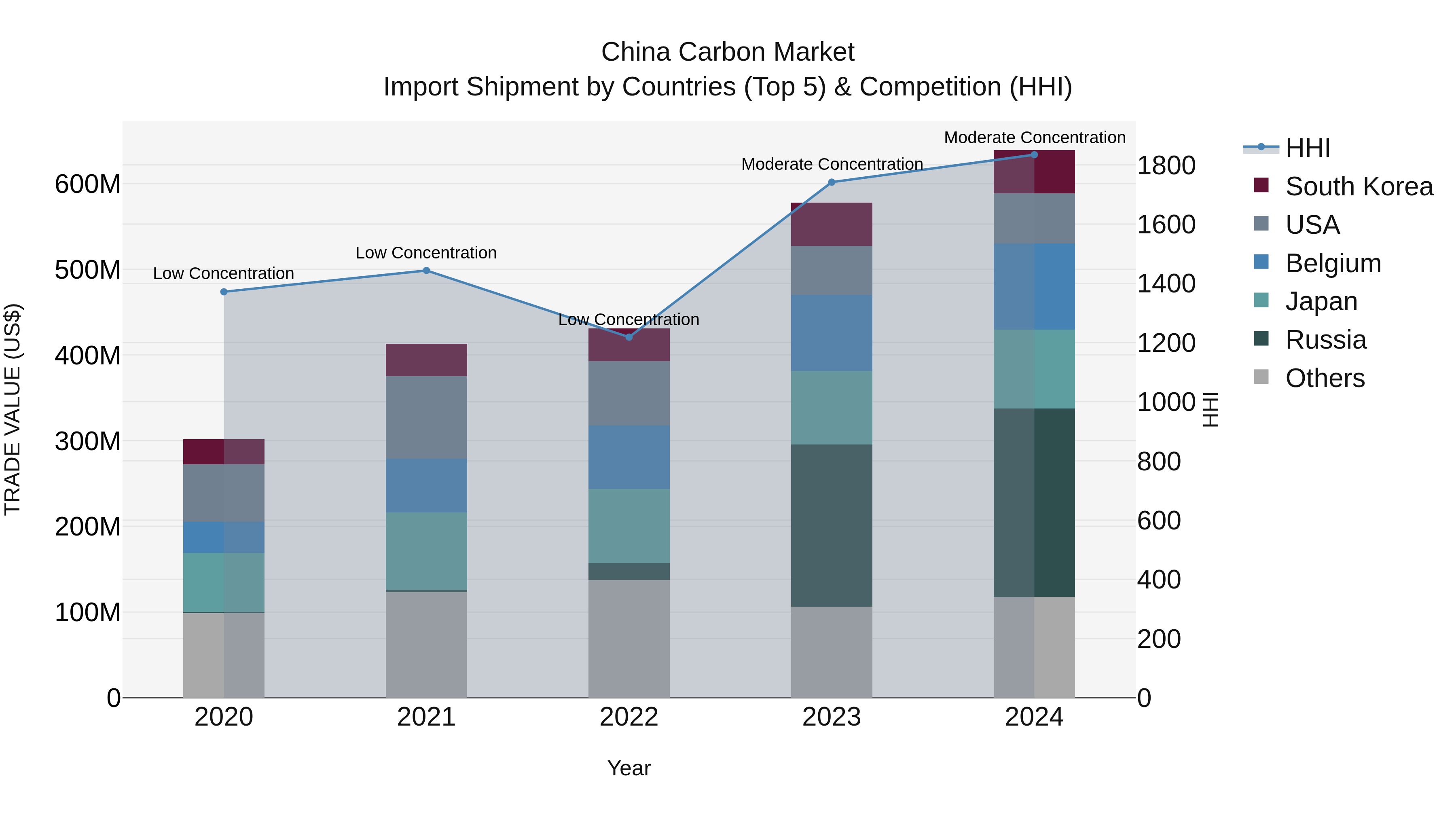

China Carbon Market Top 5 Importing Countries and Market Competition (HHI) Analysis

China carbon import shipments in 2024 saw significant growth, with top exporting countries being Russia, Belgium, Japan, USA, and South Korea. The Herfindahl-Hirschman Index (HHI) indicated moderate concentration levels, maintaining a competitive market landscape. The impressive compound annual growth rate (CAGR) of 20.64% from 2020 to 2024 highlights the expanding demand for carbon imports in China. Moreover, the growth rate of 10.64% from 2023 to 2024 demonstrates sustained momentum in the market, offering opportunities for both domestic and international suppliers to capitalize on this trend.

China Carbon Market Highlights

| Report Name | China Carbon Market |

| Forecast period | 2025-2031 |

| CAGR | 12.7% |

| Growing Sector | Automotive |

Topics Covered in the China Carbon Market Report

China Carbon Market report thoroughly covers by Product types and by Applications. The market report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high growth areas, and market drivers, which would help the stakeholders devise and align their market strategies according to the current and future.

China Carbon Market synopsis

The China carbon market is a crucial element in the nation’s strategy to reduce greenhouse gas emissions while supporting economic development. Designed to cap emissions across various sectors, it forms the backbone of China's climate objectives. The market's extensive scale and complexity mirror the country's diverse industrial landscape. As it develops, it garners significant attention for its potential influence on global climate efforts and economic transformation.

According to 6Wresearch, the China Carbon Market size is projected to grow at a compound annual growth rate (CAGR) of 12.7% during 2025–2031. This growth is fueled by strong government policies aimed at combating climate change, heightened corporate sustainability efforts, and advancements in green technology. As industries work to meet stricter emissions targets, demand for carbon credits is expected to rise sharply.

However, the market faces challenges such as regulatory inconsistencies that may create business uncertainty, varying levels of understanding and participation in carbon trading among companies, and the need for more precise monitoring and reporting systems. Economic fluctuations could also hinder investment in sustainable practices, posing additional challenges to growth. Overcoming these obstacles while leveraging the growth drivers will be critical to unlocking the full potential of China's carbon market. Therefore, sustained efforts in policy development, technological innovation, and raising business awareness and participation are vital to propelling the market forward. Additionally, international collaborations and partnerships will position China to lead in the global fight against climate change while fostering sustainable economic growth.

China Carbon Market Leading Players

Leading entities in China's carbon market include major state-owned enterprises like China National Petroleum Corporation (CNPC) and China Petroleum & Chemical Corporation (Sinopec), which play a central role in advancing emissions reduction efforts. Additionally, companies like Tesla and BYD are becoming prominent in the electric vehicle sector, significantly impacting carbon credit demand. Private firms specializing in renewable energy, such as Long Green Energy, are also instrumental in driving market growth. Moreover, technology companies offering advanced emissions tracking solutions are vital in enhancing the market's transparency and efficiency.

China Carbon Market Government Regulation

The Chinese government has enacted various measures to bolster its carbon market and advance sustainable practices. Notable policies include the launch of a national emissions trading scheme that imposes carbon caps on key industries, incentivizing reductions in greenhouse gas emissions. Additionally, financial incentives and subsidies are offered to businesses investing in clean technologies and renewable energy. The government is also focused on improving the transparency and accuracy of emissions data reporting. These initiatives are crucial for aligning corporate actions with national climate objectives and establishing a strong carbon trading framework.

Future Insight of the market

Looking forward, the China carbon market is poised for considerable growth, driven by strengthened government regulations and heightened corporate sustainability initiatives. With sustained investments in clean technologies and an increasing global emphasis on climate action, the carbon trading landscape in China is expected to advance swiftly, positioning the country as a global leader in this sector. Consequently, the market is likely to draw significant attention and investment in the years ahead. Furthermore, as China's economy continues to expand, its carbon market could serve as a blueprint for other countries aiming to balance economic growth with environmental sustainability.

Market Segmentation by Product Types

According to Dhaval, Research Manager, 6Wresearch, In the dynamic landscape of China carbon market, different product types are poised to assume key roles in market leadership. Notably, Graphite is expected to dominate, given its critical applications in batteries, especially for the rapidly growing electric vehicle sector.

Market Segmentation by Applications

In China carbon market, the Automotive industry is projected to dominate the applications category, fueled by the rising demand for electric vehicles (EVs) and the shift towards sustainable transportation solutions.

Key Attractiveness of the Report

- 10 Years Market numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year 2024

- Forecast Data until 2031.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- China Carbon Market Overview

- China Carbon Market Outlook

- Market Size of China Carbon Market, 2031

- Forecast of China Carbon Market, 2031

- Historical Data and Forecast of China Carbon Revenues & Volume for the Period 2021 – 2031

- China Carbon Market Trend Evolution

- China Carbon Market Drivers and Challenges

- China Carbon Price Trends

- China Carbon Porter's Five Forces

- China Carbon Industry Life Cycle

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Product Types for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Amorphous Carbon for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Graphite for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Diamond for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Applications for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Automotive for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Construction for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Engineering Industries for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Aerospace for the Period 2021-2031

- Historical Data and Forecast of China Carbon Market Revenues & Volume By Others for the Period 2021-2031

- China Carbon Import Export Trade Statistics

- Market Opportunity Assessment By Product Types

- Market Opportunity Assessment By Applications

- China Carbon Top Companies Market Share

- China Carbon Competitive Benchmarking By Technical and Operational Parameters

- China Carbon Company Profiles

- China Carbon Key Strategic Recommendations

Markets Covered

The China Carbon market report provides a detailed analysis of the following market segments.

By Product Types

- Amorphous Carbon

- Graphite

- Diamond

By Applications

- Automotive

- Construction

- Engineering Industries

- Aerospace

- Others

China Carbon Market (2025-2031): FAQs

The China carbon market is projected to grow at a compound annual growth rate (CAGR) of 12.7% from 2025 to 2031, driven by supportive government policies and increasing corporate sustainability initiatives.

Key challenges include regulatory inconsistencies, varying levels of comprehension among businesses, and economic fluctuations that could hinder investment in sustainable practices.

Ongoing advancements in green technology and heightened awareness of emission reduction strategies will be critical in shaping market dynamics and enhancing engagement from industries.

The Chinese government is implementing robust policies aimed at climate mitigation, which are essential for fostering a conducive environment for corporate sustainability and emissions reduction.

6Wresearch actively monitors the China Carbon Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Carbon Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1. Executive Summary |

| 2. Introduction |

| 2.1. Key Highlights of the Report |

| 2.2. Report Description |

| 2.3. Market Scope & Segmentation |

| 2.4. Research Methodology |

| 2.5. Assumptions |

| 3. China Carbon Market Overview |

| 3.1. China Country Macro Economic Indicators |

| 3.2. China Carbon Market Revenues & Volume, 2021 & 2031F |

| 3.3. China Carbon Market - Industry Life Cycle |

| 3.4. China Carbon Market - Porter's Five Forces |

| 3.5. China Carbon Market Revenues & Volume Share, By Product Types, 2021 & 2031F |

| 3.6. China Carbon Market Revenues & Volume Share, By Applications, 2021 & 2031F |

| 4. China Carbon Market Dynamics |

| 4.1. Impact Analysis |

| 4.2. Market Drivers |

| 4.2.1 Implementation of government policies and regulations promoting carbon emission reduction. |

| 4.2.2 Growing awareness and concern about environmental sustainability among businesses and consumers. |

| 4.2.3 Increased adoption of carbon trading and offset programs by companies to comply with regulatory requirements. |

| 4.3. Market Restraints |

| 4.3.1 Lack of transparency and consistency in carbon pricing mechanisms. |

| 4.3.2 Uncertainty surrounding future government policies and regulations related to carbon emissions. |

| 4.3.3 Potential market manipulation and fraud in carbon trading activities. |

| 5. China Carbon Market Trends |

| 6. China Carbon Market, By Types |

| 6.1. China Carbon Market, By Product Types |

| 6.1.1 Overview and Analysis |

| 6.1.2. China Carbon Market Revenues & Volume, By Product Types, 2021-2031F |

| 6.1.3. China Carbon Market Revenues & Volume, By Amorphous Carbon, 2021-2031F |

| 6.1.4. China Carbon Market Revenues & Volume, By Graphite, 2021-2031F |

| 6.1.5. China Carbon Market Revenues & Volume, By Diamond, 2021-2031F |

| 6.2. China Carbon Market, By Applications |

| 6.2.1. Overview and Analysis |

| 6.2.2. China Carbon Market Revenues & Volume, By Automotive, 2021-2031F |

| 6.2.3. China Carbon Market Revenues & Volume, By Construction, 2021-2031F |

| 6.2.4. China Carbon Market Revenues & Volume, By Engineering Industries, 2021-2031F |

| 6.2.5. China Carbon Market Revenues & Volume, By Aerospace, 2021-2031F |

| 6.2.6. China Carbon Market Revenues & Volume, By Others, 2021-2031F |

| 7. China Carbon Market Import-Export Trade Statistics |

| 7.1 China Carbon Market Export to Major Countries |

| 7.2. China Carbon Market Imports from Major Countries |

| 8. China Carbon Market Key Performance Indicators |

| 8.1 Carbon credit prices in the market. |

| 8.2 Number of companies participating in carbon trading and offset programs. |

| 8.3 Carbon emissions reductions achieved through market initiatives. |

| 8.4 Percentage of renewable energy sources in China's energy mix. |

| 8.5 Number of carbon market transactions and volumes traded. |

| 9. China Carbon Market - Opportunity Assessment |

| 9.1. China Carbon Market Opportunity Assessment, By Product Types, 2021 & 2031F |

| 9.2. China Carbon Market Opportunity Assessment, By Applications, 2021 & 2031F |

| 10. China Carbon Market - Competitive Landscape |

| 10.1. China Carbon Market Revenue Share, By Companies, 2024 |

| 10.2. China Carbon Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11. Company Profiles |

| 12. Recommendations |

| 13. Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026 - 2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

- Saudi Arabia Car Window Tinting Film, Paint Protection Film (PPF), and Ceramic Coating Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero