France Orthopedic Devices Market Outlook | Share, Growth, Value, Size, Industry, COVID-19 IMPACT, Analysis, Forecast, Companies, Trends & Revenue

Market Forecast By Application (Hip Orthopedic Devices, Knee Orthopedic Devices, Spine Orthopedic Devices, Craniomaxillofacial Orthopedic Devices, Dental Orthopedic Devices, Sports Injuries, Extremities And Trauma (Set) Orthopedic Devices), By Product (Drill Guide, Guide Tubes, Implant Holder, Custom Clamps, Distracters, Screw Drivers, Accessories) And Competitive Landscape

| Product Code: ETC368110 | Publication Date: Aug 2022 | Updated Date: Nov 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Sachin Kumar Rai | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

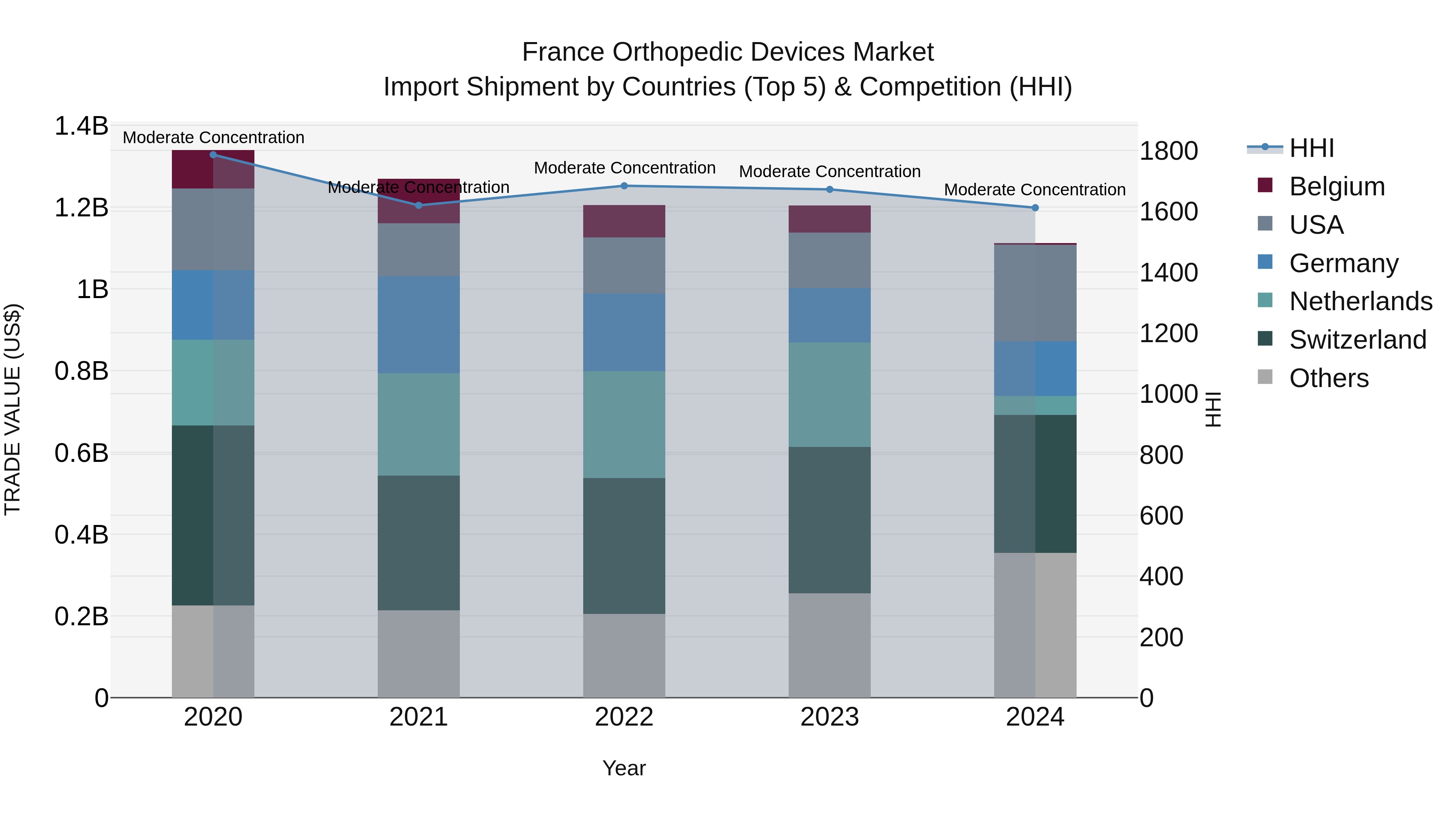

France Orthopedic Devices Market Top 5 Importing Countries and Market Competition (HHI) Analysis

In 2024, France saw a steady flow of orthopedic devices imports, with key exporters including Switzerland, USA, Germany, Netherlands, and Italy. Despite a negative Compound Annual Growth Rate (CAGR) of -4.54% from 2020 to 2024 and a decline in growth rate from 2023 to 2024, the Herfindahl-Hirschman Index (HHI) indicated moderate concentration within the market. This suggests a stable market environment for orthopedic devices in France, with continued reliance on top exporting countries for quality products.

France Orthopedic Devices Market Synopsis

The France Orthopedic Devices Market is a dynamic and competitive industry that encompasses a wide range of products including joint reconstruction implants, spinal devices, orthobiologics, orthopedic braces and supports, and trauma fixation devices. The market is driven by factors such as the increasing prevalence of musculoskeletal disorders, growing aging population, advancements in technology leading to innovative product development, and the rise in sports-related injuries. Key players in the market include Medtronic, Stryker Corporation, Zimmer Biomet Holdings, Inc., and DePuy Synthes. Regulatory reforms and reimbursement policies play a crucial role in shaping the market landscape. The market is expected to continue its growth trajectory due to the rising demand for minimally invasive procedures and the focus on improving patient outcomes through technological advancements.

France Orthopedic Devices Market Trends

The France Orthopedic Devices Market is experiencing several key trends currently. One significant trend is the increasing demand for minimally invasive orthopedic procedures and devices, driven by the benefits of faster recovery times, reduced scarring, and less post-operative pain for patients. Another notable trend is the growing adoption of advanced technologies such as 3D printing and robotic-assisted surgeries in orthopedics, leading to more personalized and precise treatment options. Additionally, there is a focus on developing innovative materials and implants to improve the durability and longevity of orthopedic devices. The market is also witnessing a rise in the geriatric population, contributing to the demand for orthopedic devices to address age-related musculoskeletal conditions. Overall, these trends are shaping the landscape of the France Orthopedic Devices Market towards more efficient, technologically advanced, and patient-centric solutions.

France Orthopedic Devices Market Challenges

In the France Orthopedic Devices Market, challenges include increasing competition from both domestic and international players, stringent regulations and reimbursement policies, and the rising costs of research and development for innovative products. Additionally, there is a growing demand for personalized and technologically advanced orthopedic devices, putting pressure on companies to continuously invest in R&D to meet evolving customer needs. Moreover, the impact of the COVID-19 pandemic has disrupted supply chains and delayed elective surgeries, affecting the overall market growth. Adapting to these challenges requires companies to focus on product differentiation, regulatory compliance, cost management, and strategic partnerships to stay competitive in the dynamic France Orthopedic Devices Market.

France Orthopedic Devices Market Investment Opportunities

The France Orthopedic Devices Market presents several promising investment opportunities due to factors such as the aging population, increasing prevalence of orthopedic disorders, and technological advancements in the field. With a growing demand for orthopedic devices such as joint implants, prosthetics, and orthobiologics, investors can consider opportunities in companies specializing in innovative products and solutions. Additionally, the market is witnessing a shift towards minimally invasive procedures and personalized orthopedics, opening up avenues for investments in cutting-edge technologies and services. Collaborations with healthcare institutions and research organizations to develop next-generation orthopedic devices could also be a strategic investment approach in this evolving market landscape.

Jordan Agar Market Government Policies

In France, the Orthopedic Devices Market is regulated by various government policies aimed at ensuring patient safety and product quality. The regulatory framework is primarily overseen by the French National Agency for Medicines and Health Products Safety (ANSM), which evaluates and approves orthopedic devices for market entry. Additionally, the European Medical Devices Regulation (MDR) sets out stringent requirements for the manufacturing, distribution, and marketing of orthopedic devices within the European Union, including France. Companies operating in this market must comply with these regulations to obtain necessary approvals and maintain market access. The government policies emphasize transparency, traceability, and quality control measures to safeguard patient health and promote innovation in the orthopedic devices sector in France.

France Orthopedic Devices Market Future Outlook

The future outlook for the France Orthopedic Devices Market appears positive, driven by factors such as the aging population, increasing prevalence of orthopedic disorders, and advancements in technology leading to the development of innovative products. The market is expected to witness steady growth as demand for orthopedic devices such as joint implants, prosthetics, and orthobiologics continues to rise. Additionally, the growing adoption of minimally invasive surgical procedures and the focus on improving patient outcomes and reducing healthcare costs are likely to further propel market expansion. However, challenges such as pricing pressures, regulatory hurdles, and competition from alternative therapies may impact market growth to some extent. Overall, the France Orthopedic Devices Market is poised for growth in the coming years, presenting opportunities for market players to innovate and expand their presence.

Key Highlights of the Report:

- France Orthopedic Devices Market Outlook

- Market Size of France Orthopedic Devices Market, 2021

- Forecast of France Orthopedic Devices Market, 2031

- Historical Data and Forecast of France Orthopedic Devices Revenues & Volume for the Period 2018 - 2031

- France Orthopedic Devices Market Trend Evolution

- France Orthopedic Devices Market Drivers and Challenges

- France Orthopedic Devices Price Trends

- France Orthopedic Devices Porter's Five Forces

- France Orthopedic Devices Industry Life Cycle

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Application for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Hip Orthopedic Devices for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Knee Orthopedic Devices for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Spine Orthopedic Devices for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Craniomaxillofacial Orthopedic Devices for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Dental Orthopedic Devices for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Sports Injuries, Extremities And Trauma (Set) Orthopedic Devices for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Product for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Drill Guide for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Guide Tubes for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Implant Holder for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Custom Clamps for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Distracters for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Screw Drivers for the Period 2018 - 2031

- Historical Data and Forecast of France Orthopedic Devices Market Revenues & Volume By Accessories for the Period 2018 - 2031

- France Orthopedic Devices Import Export Trade Statistics

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By Product

- France Orthopedic Devices Top Companies Market Share

- France Orthopedic Devices Competitive Benchmarking By Technical and Operational Parameters

- France Orthopedic Devices Company Profiles

- France Orthopedic Devices Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the France Orthopedic Devices Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the France Orthopedic Devices Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- China Electric Appliance Rental Market (2026-2032) | Trends, Revenue, Growth, Challenges, Size, Value, Outlook, Pricing, Strategy, Insights, Restraints, segmentation, Companies, Investment Opportunities, Analysis, Demand, Drivers, Competition, Forecast, Share

- Chile Electric Appliance Rental Market (2026-2032) | Outlook, Competition, Drivers, Strategy, Revenue, Analysis, Value, Pricing, Restraints, Size, Demand, Share, Growth, Forecast, Challenges, Insights, Investment Opportunities, Companies, Trends, segmentation

- Cambodia Electric Appliance Rental Market (2026-2032) | Companies, Analysis, Restraints, Pricing, Insights, Challenges, Outlook, Strategy, Forecast, Trends, Competition, Value, Revenue, Investment Opportunities, segmentation, Drivers, Size, Demand, Growth, Share

- Brazil Electric Appliance Rental Market (2026-2032) | Revenue, Strategy, Forecast, Companies, segmentation, Competition, Size, Investment Opportunities, Pricing, Restraints, Outlook, Challenges, Analysis, Drivers, Value, Demand, Insights, Trends, Growth, Share

- Bangladesh Electric Appliance Rental Market (2026-2032) | Drivers, Forecast, Investment Opportunities, Strategy, Insights, Demand, Challenges, Outlook, Trends, Competition, Value, Revenue, Size, Pricing, Analysis, Companies, Restraints, segmentation, Share, Growth

- Bahrain Electric Appliance Rental Market (2026-2032) | Outlook, Size, Competition, Restraints, Drivers, Value, Trends, Investment Opportunities, Insights, Forecast, Revenue, Strategy, Growth, Share, Demand, Analysis, Challenges, Companies, segmentation, Pricing

- Azerbaijan Electric Appliance Rental Market (2026-2032) | Trends, Investment Opportunities, Restraints, Insights, Strategy, Competition, Value, Growth, Demand, Drivers, Analysis, Forecast, Size, Share, Outlook, segmentation, Pricing, Challenges, Revenue, Companies

- Australia Electric Appliance Rental Market (2026-2032) | Challenges, Restraints, Forecast, Demand, Size, Competition, Pricing, Investment Opportunities, Revenue, Trends, Drivers, Growth, Outlook, Analysis, Strategy, Value, segmentation, Insights, Companies, Share

- Argentina Electric Appliance Rental Market (2026-2032) | Growth, Trends, Insights, Outlook, Forecast, Size, Drivers, Analysis, Restraints, Challenges, Share, Revenue, Investment Opportunities, Strategy, Demand, Value, Companies, segmentation, Competition, Pricing

- Algeria Electric Appliance Rental Market (2026-2032) | Share, Size, Value, Strategy, Competition, Outlook, Challenges, Companies, Trends, Pricing, Insights, Forecast, Investment Opportunities, Revenue, Growth, Restraints, segmentation, Analysis, Demand, Drivers

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero