India Candy Market (2025-2031) | Growth, Share, Companies, Revenue, Forecast, Trends, Size, Industry, Value & Analysis

Market Forecast By Product Type (Chocolate Candy, Non-Chocolate Candy), By Distribution (Supermarkets and Hypermarkets, Convenience Stores, Specalist Retailers, Online Retail, Others) And Competitive Landscape

| Product Code: ETC040145 | Publication Date: Aug 2023 | Updated Date: Nov 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

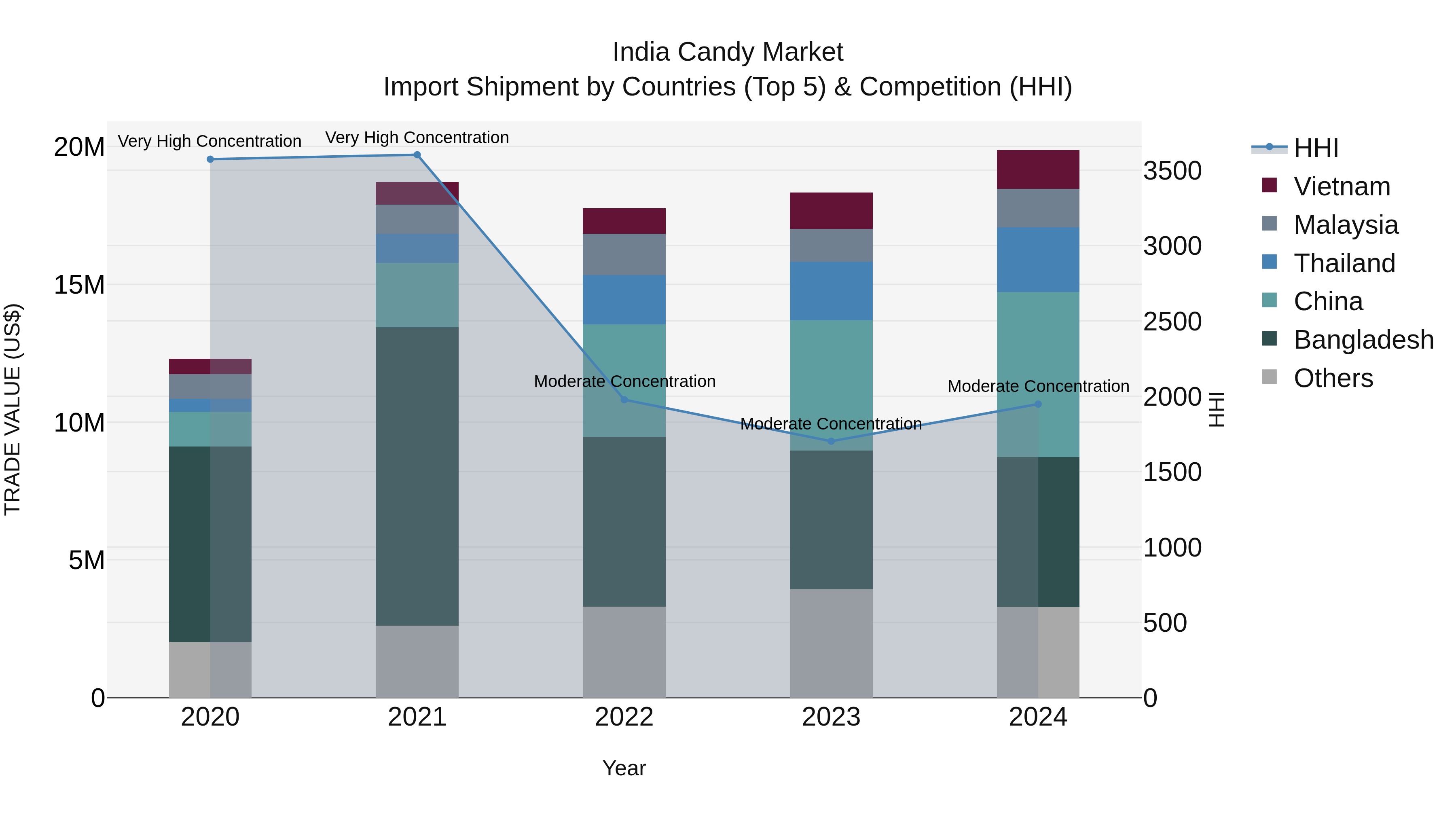

India Candy Market Import Shipment by Countries (Top 5) & Competition (HHI)

India's candy import shipments in 2024 saw significant contributions from top exporting countries such as China, Bangladesh, Thailand, Malaysia, and Vietnam. Despite the moderate concentration in the market, the Compound Annual Growth Rate (CAGR) from 2020 to 2024 stood at an impressive 12.75%. The growth rate from 2023 to 2024 was also notable at 8.42%, indicating a positive trend in the import market for candies in India. This data suggests a growing demand for imported candies among Indian consumers, with key countries playing a vital role in meeting this demand.

India Candy Market Growth Rate

According to 6Wresearch internal database and industry insights, the India Candy Market is growing at a compound annual growth rate (CAGR) of 7.4% during the forecast period (2025–2031).

India Candy Market Highlights

| Report Name | India Candy Market |

| Forecast Period | 2025-2031 |

| CAGR | 7.4% |

| Growing Sector | Residential Sector |

Topics Covered in the India Candy Market Report

The India Candy Market report thoroughly covers the market by product type and distribution channel. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders devise and align their market strategies according to the current and future market dynamics.

India Candy Market Synopsis

The India Candy Market is expected to see steady growth. The market is driven by rising demand for convenience indulgence products driven by urbanisation, higher disposable incomes, and growth of modern retail and online channels. Also, increasing product innovation (flavours, formats), growing adult consumption, and better availability across tier-2/3 cities are helping propel market growth. The organised candy (confectionery) sector is benefitting from global and domestic players scaling up, and with tie-ups, flavour-led innovation, and targeted marketing. Government support in F&B processing, modern retail infrastructure, and cold-chain/logistics investments also play a supportive role.

Evaluation of Growth Drivers in the India Candy Market

Below mentioned some growth drivers and their impact on market dynamics:

| Drivers | Primary Segments Affected | Why It Matters |

| Urbanisation & Busy Lifestyles | Product Type (Chocolate Candy, Non-Chocolate Candy) | Creates demand for on-the-go indulgence and impulse purchases. |

| Rising Disposable Income | Distribution (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Others) | More spending power means premium/fun segments gain traction. |

| Product Innovation & Format Variety | Product Type | Novel flavours, premium formats attract consumers beyond children. |

| Expansion of Modern Retail & E-commerce | Distribution Channels | Better accessibility across geographies, ease of purchase. |

| Processing & Supply-Chain Improvements | Distribution, Product Type | Allows better product availability, tier-2/3 reach, refresh packaging. |

The India Candy Market is projected to grow significantly at a compound annual growth rate CAGR of 7.4% during the forecast period of 2025 to 2031. Growth is driven by increasing consumption of confectionery in both children and adult segments, growing preference for novel candy formats, and better reach of modern retail and online. Urban and semi-urban regions are key growth areas. The proliferation of convenience stores, supermarkets/hypermarkets, and online home-delivery platforms is expanding the consumer base for candy products. Improvements in manufacturing, packaging, flavour innovation, and supply chains also improve market quality and reach.

Evaluation of Restraints in the India Candy Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segments Affected | What This Means |

| Health concerns & sugar reduction trends | Product Type (Chocolate Candy, Non-Chocolate Candy) | Reduced sugar and health-driven avoidance may limit growth of traditional candy forms. |

| Intense competition & low entry barriers | All Segments | Many local players, small margins; pricing pressure and shelf-space wars. |

| Regulatory & labelling requirements (additives, colours) | All Segments | Additional cost and complexity for manufacturers to comply with e.g. Food Safety and Standards Authority of India (FSSAI) guidelines. |

| Price sensitivity in mass market | Distribution & Product Type | consumers in tier-2/3 cities are price sensitive; premiumisation is constrained. |

| Reliance on festival/seasonal demand | Distribution, Product Type | Sales may spike seasonally (festivals) and then decline, affecting steady growth. |

India Candy Market Challenges

India Candy Market is under pressure due to consumers moving toward healthier, low-sugar snacks, which impacts demand for traditional offerings. The market structure is fragmented, and strong competition from global and local players limits margins. Volatility in sugar and flavor prices adds further cost challenges. In addition, the sector struggles with low reach in rural and remote areas, and distribution and logistics issues hinder seamless product availability, restricting the overall market expansion.

India Candy Market Trends

Some major trends contributing to development of the India Candy Market growth are:

- Premium & Novel Formats: Growth of premium candy formats (liquid-filled, flavour bursts, novelty shapes) appealing to adult consumers and gifting occasions.

- Health-Focused Variants: launch of sugar-free, reduced-sugar, clean-label candy options to cater to health-conscious consumers.

- Modern Retail & E-commerce Expansion: growth of supermarkets/hypermarkets, convenience stores, and online grocery and impulse-buy platforms improving availability.

- Localization & Regional Flavours: candy brands adopting local flavours, regional tastes and formats (e.g., tangy, masala, fruit) to appeal across India.

- Impulse & Gifting Usage Growth: growing usage of candy as gifting items, celebrations, and impulse purchases beyond children’s treats.

Investment Opportunities in the India Candy Industry

Here are some investment opportunities in the India candy industry:

- Expanding Modern Retail and E-Commerce Presence: Build partnerships and distribution to increase candy availability in stores and online.

- Innovation in Healthy & Premium Candy Products: create low-sugar, functional, or premium candies for adults and gifting occasions.

- Regional Flavour & Formats Development: Develop products with local tastes and cost-effective formats for tier-2/3 markets.

- Supply-Chain & Packaging Upgrades: improve production, packaging, and logistics to reach semi-urban and rural areas efficiently.

- Brand Building & Experience-Led Promotions: Strengthen brand visibility via retail, online marketing, and festive or gifting campaigns.

Top 5 Leading Players in the India Candy Market

Here are some top companies contributing to India Candy Market share:

1. DS Group

| Market Name | DS Group |

| Established Year | 1929 |

| Headquarters | New Delhi, India |

| Official Website | - |

DS Group is a major player in India’s candy market, especially hard-boiled candy and ethnic confectionery. The company’s brands like “Pulse” dominate the hard-boiled segment.

2. Perfetti Van Melle India Pvt. Ltd.

| Market Name | Perfetti Van Melle India Pvt. Ltd. |

| Established Year | 1988 |

| Headquarters | Gurugram, India |

| Official Website | Click Here |

A leading international candy company in India, offering brands like Alpenliebe, Mentos, Fruittella, known for flavour-centric innovation and strong youth appeal.

3. Nestlé India Ltd.

| Market Name | Nestlé India Ltd. |

| Established Year | 1988 |

| Headquarters | Gurugram, India |

| Official Website | Click Here |

While more known for chocolate and confectionery broadly, Nestlé has candy offerings and strong distribution presence across India, supporting its candy business in urban markets.

4. Lotte India Corporation Ltd.

| Market Name | Lotte India Corporation Ltd. |

| Established Year | 2013 (though roots earlier) |

| Headquarters | Chennai, India |

| Official Website | - |

Lotte India is involved in confectionery including candies and is expanding capacity and turnover significantly in recent years.

5. ITC Ltd.

| Market Name | ITC Ltd. |

| Established Year | 1910 |

| Headquarters | Kolkata, India |

| Official Website | Click Here |

ITC has a diversified portfolio in FMCG including confectionery/candy products; its wide distribution and brand strength make it an important player in the candy market.

Government Regulations Introduced in the India Candy Market

According to Indian Government Data, rules significantly influence the development of the candy market. The Food Safety and Standards Authority of India (FSSAI) oversees confectionery ingredients, additives, production standards, and labeling, promoting' the safety of candy products for consumption. The Indian government has enacted initiatives to enhance food product processing, including the “Cold Chain, Value Addition and Preservation Infrastructure” scheme and the “PM FME (Prime Minister’s Formalisation of Micro Food Processing Enterprises),” which have improved candy manufacturing and expanded distribution.

Future Insights of the India Candy Market

The outlook for the India Candy Market appears favourable, with steady growth forecasts. The market is propelled by rising consumption of candy across age groups, growing urbanisation, and increasing penetration into tier-2/3 markets. The rising demand for innovative candy formats and healthier variants will persist in driving market growth. The proliferation of online retail, convenience store chains, and home-delivery for confectionery will facilitate further expansion. Government actions designed to promote food processing infrastructure and support small-medium enterprises will also improve the market picture.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Non-Chocolate Candy to Dominate the Market - By Product Type

According to Guneet Kaur, Senior Research Analyst, 6Wresearch, non-chocolate candy is the fastest-growing segment due to its wide appeal among children and adults. The variety of flavors and formats, including lollipops and jellies, makes it highly preferred for impulse purchases and gifting occasions.

Supermarkets and Hypermarkets to Dominate the Market – By Distribution Channel

The supermarkets and hypermarkets segment is growing rapidly as it provides wide availability of diverse candy types under one roof. Customers prefer these stores for bulk buying, variety, and convenience, which significantly supports the expansion of organized retail distribution in India.

Key attractiveness of the report

- 10 Years Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024

- Forecast Data until 2031.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- India Candy Market Outlook

- Market Size of India Candy Market, 2024

- Forecast of India Candy Market, 2031

- Historical Data and Forecast of India Candy Revenues & Volume for the Period 2021-2031

- India Candy Market Trend Evolution

- India Candy Market Drivers and Challenges

- India Candy Price Trends

- India Candy Porter's Five Forces

- India Candy Industry Life Cycle

- Historical Data and Forecast of India Candy Market Revenues & Volume By Product Type for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Chocolate Candy for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Non-Chocolate Candy for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Distribution for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Supermarkets and Hypermarkets for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Convenience Stores for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Specalist Retailers for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Online Retail for the Period 2021-2031

- Historical Data and Forecast of India Candy Market Revenues & Volume By Others for the Period 2021-2031

- India Candy Import Export Trade Statistics

- Market Opportunity Assessment By Product Type

- Market Opportunity Assessment By Distribution

- India Candy Top Companies Market Share

- India Candy Competitive Benchmarking By Technical and Operational Parameters

- India Candy Company Profiles

- India Candy Key Strategic Recommendations

Market covered

The report subsequently covers the market by following segments and subsegments.

By Product Type

- Chocolate Candy

- Non-Chocolate Candy

By Distribution

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Retail

- Others

India Candy Market (2025-2031) : FAQ's

The India Candy Market is projected to grow at 7.4% CAGR during the forecast period of 2025-2031.

Non-chocolate candy and supermarkets/hypermarkets drive the India Candy Market growth.

Urbanization, higher incomes, flavor innovation, modern retail, and online channels boost India Candy Market growth.

Health trends, competition, regulations, price sensitivity, and rural reach challenge India Candy Market growth.

Premium formats, health-focused variants, retail expansion, local flavors, and gifting drive India Candy Market trends.

6Wresearch actively monitors the India Candy Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the India Candy Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 India Candy Market Overview |

| 3.1 India Country Macro Economic Indicators |

| 3.2 India Candy Market Revenues & Volume, 2021 & 2031F |

| 3.3 India Candy Market - Industry Life Cycle |

| 3.4 India Candy Market - Porter's Five Forces |

| 3.5 India Candy Market Revenues & Volume Share, By Product Type, 2021 & 2031F |

| 3.6 India Candy Market Revenues & Volume Share, By Distribution, 2021 & 2031F |

| 4 India Candy Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income of consumers in India |

| 4.2.2 Growing popularity of gifting candies on various occasions |

| 4.2.3 Rising demand for innovative and premium candy products |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating prices of raw materials such as sugar and flavors |

| 4.3.2 Intense competition from other snack and confectionery products in the market |

| 5 India Candy Market Trends |

| 6 India Candy Market, By Types |

| 6.1 India Candy Market, By Product Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 India Candy Market Revenues & Volume, By Product Type, 2021-2031F |

| 6.1.3 India Candy Market Revenues & Volume, By Chocolate Candy, 2021-2031F |

| 6.1.4 India Candy Market Revenues & Volume, By Non-Chocolate Candy, 2021-2031F |

| 6.2 India Candy Market, By Distribution |

| 6.2.1 Overview and Analysis |

| 6.2.2 India Candy Market Revenues & Volume, By Supermarkets and Hypermarkets, 2021-2031F |

| 6.2.3 India Candy Market Revenues & Volume, By Convenience Stores, 2021-2031F |

| 6.2.4 India Candy Market Revenues & Volume, By Specalist Retailers, 2021-2031F |

| 6.2.5 India Candy Market Revenues & Volume, By Online Retail, 2021-2031F |

| 6.2.6 India Candy Market Revenues & Volume, By Others, 2021-2031F |

| 7 India Candy Market Import-Export Trade Statistics |

| 7.1 India Candy Market Export to Major Countries |

| 7.2 India Candy Market Imports from Major Countries |

| 8 India Candy Market Key Performance Indicators |

| 8.1 Consumer engagement on social media platforms for candy brands |

| 8.2 Number of new product launches and innovations in the candy market |

| 8.3 Growth in online sales and e-commerce penetration for candy products |

| 9 India Candy Market - Opportunity Assessment |

| 9.1 India Candy Market Opportunity Assessment, By Product Type, 2021 & 2031F |

| 9.2 India Candy Market Opportunity Assessment, By Distribution, 2021 & 2031F |

| 10 India Candy Market - Competitive Landscape |

| 10.1 India Candy Market Revenue Share, By Companies, 2024 |

| 10.2 India Candy Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Related Reports

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

- Saudi Arabia Car Window Tinting Film, Paint Protection Film (PPF), and Ceramic Coating Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- South Africa Stationery Market (2025-2031) | Share, Size, Industry, Value, Growth, Revenue, Analysis, Trends, Segmentation & Outlook

- Afghanistan Rocking Chairs And Adirondack Chairs Market (2026-2032) | Size & Revenue, Competitive Landscape, Share, Segmentation, Industry, Value, Outlook, Analysis, Trends, Growth, Forecast, Companies

- Afghanistan Apparel Market (2026-2032) | Growth, Outlook, Industry, Segmentation, Forecast, Size, Companies, Trends, Value, Share, Analysis & Revenue

- Canada Oil and Gas Market (2026-2032) | Share, Segmentation, Value, Industry, Trends, Forecast, Analysis, Size & Revenue, Growth, Competitive Landscape, Outlook, Companies

Industry Events and Analyst Meet

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Stationery & Paper Expo Saudi Arabia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero