Indonesia Urea Market (2025-2031) Outlook | Analysis, Size, Trends, Value, Forecast, Industry, Growth, Companies, Share & Revenue

Market Forecast By Grade (Fertilizer, Feed, Technical), By End-user Industry (Agriculture, Chemical, Automotive, Medical, Others) And Competitive Landscape

| Product Code: ETC211000 | Publication Date: Jul 2023 | Updated Date: Feb 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 60 | No. of Figures: 40 | No. of Tables: 7 |

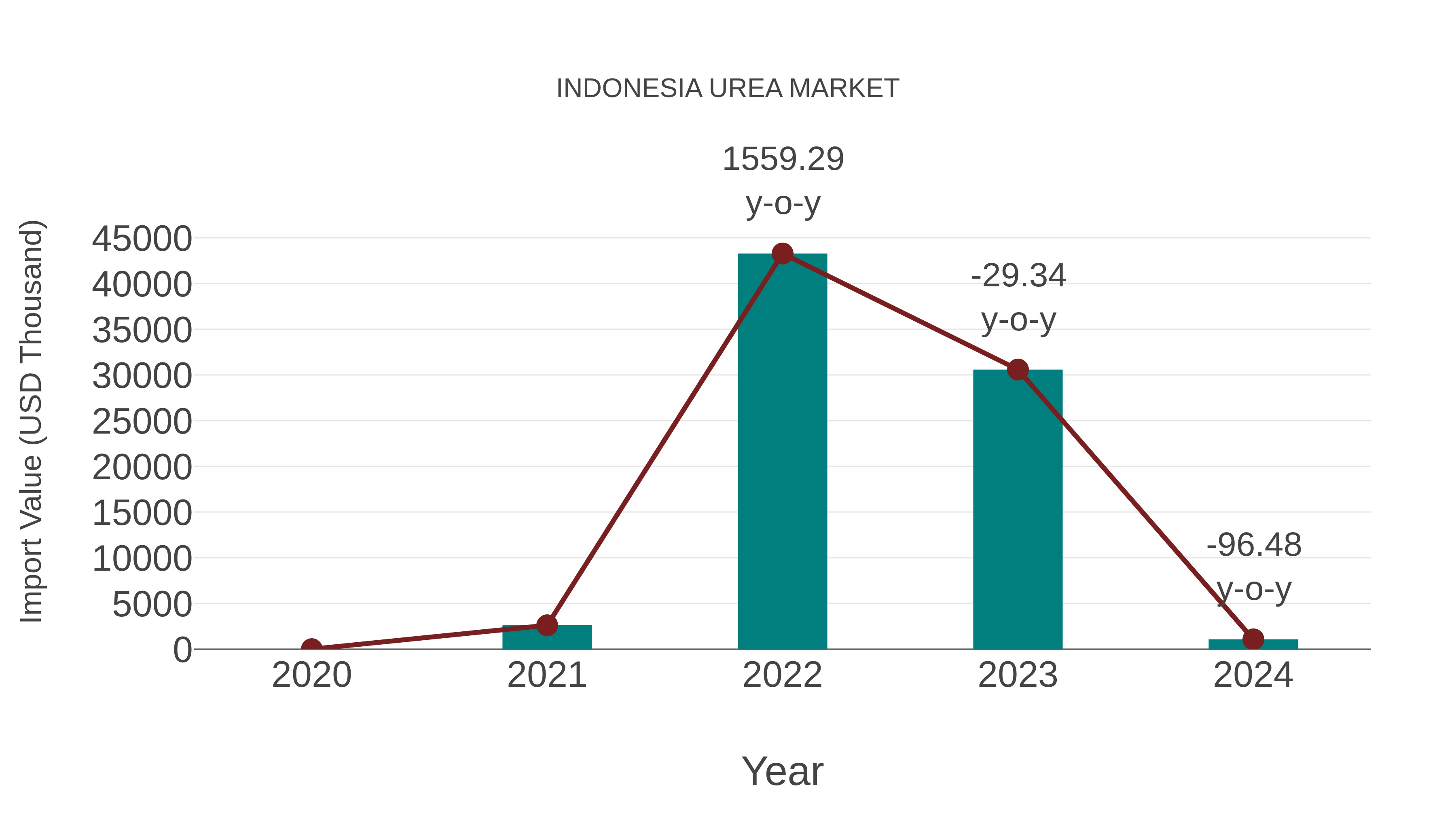

Indonesia Urea Market: Import Trend Analysis

In the Indonesia urea market, the import trend experienced a significant decline from 2023 to 2024, with a notable -96.48% growth rate. The compound annual growth rate (CAGR) for imports between 2020 and 2024 stood at -25.56%. This sharp decrease could be attributed to shifts in demand dynamics or changes in trade policies impacting market stability.

Indonesia Urea MarketSynopsis

Indonesia is the world?s largest importer of urea, with imports reaching 9.5 million tons in 2025. Urea is a key component of the fertilizer industry in Indonesia and plays an essential role in maintaining agricultural output. The Indonesia urea market has experienced significant growth over recent years due to increasing demand for agricultural production and rising government investments into the country`s agriculture sector.

Market Trends

The demand for urea in Indonesia is expected to continue growing at a steady rate due to increasing government investments into its agriculture sector as well as rising domestic food consumption needs. Additionally, new players are entering the market, such as China-based companies looking to capitalize on cheap imported products from India and other countries that could potentially disrupt the local market share held by incumbent firms. Furthermore, technological advancements have enabled more efficient production processes while also boosting product quality standards which should drive further demand growth going forward.

Market Drivers

Some of the main drivers behind the growth of Indonesia urea market include increased investment in infrastructure projects related to agriculture which will lead to higher crop yields; introduction of new technologies such as precision farming; expansion of irrigation systems; development of safe storage facilities for storing harvested crops and access to better inputs like fertilizers including urea; improved transport networks connecting farmers with markets; greater availability/accessibility of credit facilities enabling farmers purchase necessary inputs etc. All these factors are likely to contribute towards stronger growth prospects within this segment over coming years.

COVID-19 Impact on the Market

Due COVID-19 pandemic situation there were issues regarding logistics & transportation leading disruption supply chain particularly affecting shipments from major suppliers like China & India which resulted into shortage across various regions. As a result prices grew too high causing negative impact on residential end users having limited budgets making it difficult for them buy agrochemicals like Urea. Government efforts eventually helped restore normalcy but still many rural areas facing problems caused due lockdown restrictions. This has impacted overall sales & profitability across industries involving agrochemicals including UREA.

Challenges of the Market

Despite positive outlook , some challenges remain that can impede further progress specially pertainingto import regulations causing delays in delivery times , lack modernized distribution system apart from outdated logistic network resulting post Brexit changes creating disruptions especially those concerning exports resulting complications arising out large number bureaucratic procedures required before any shipment takes place alongwith currency fluctuations impacting value addition process etc.

Industry Key Players

The Indonesia urea market is heavily influenced by import substitution policies, government subsidies, and the availability of cheap natural gas. The key players in the Indonesia Urea Market are PT Pupuk Sriwijaya (PUSRI), PT Petrokimia Gresik, Yara International ASA, and PhosAgro.

Key Highlights of the Report:

- Indonesia Urea Market Outlook

- Market Size of Indonesia Urea Market, 2024

- Forecast of Indonesia Urea Market, 2031

- Historical Data and Forecast of Indonesia Urea Revenues & Volume for the Period 2021-2031

- Indonesia Urea Market Trend Evolution

- Indonesia Urea Market Drivers and Challenges

- Indonesia Urea Price Trends

- Indonesia Urea Porter's Five Forces

- Indonesia Urea Industry Life Cycle

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Grade for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Fertilizer for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Feed for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Technical for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By End-user Industry for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Agriculture for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Chemical for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Automotive for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Medical for the Period 2021-2031

- Historical Data and Forecast of Indonesia Urea Market Revenues & Volume By Others for the Period 2021-2031

- Indonesia Urea Import Export Trade Statistics

- Market Opportunity Assessment By Grade

- Market Opportunity Assessment By End-user Industry

- Indonesia Urea Top Companies Market Share

- Indonesia Urea Competitive Benchmarking By Technical and Operational Parameters

- Indonesia Urea Company Profiles

- Indonesia Urea Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Indonesia Urea Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Indonesia Urea Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Indonesia Urea Market Overview |

3.1 Indonesia Country Macro Economic Indicators |

3.2 Indonesia Urea Market Revenues & Volume, 2021 & 2031F |

3.3 Indonesia Urea Market - Industry Life Cycle |

3.4 Indonesia Urea Market - Porter's Five Forces |

3.5 Indonesia Urea Market Revenues & Volume Share, By Grade, 2021 & 2031F |

3.6 Indonesia Urea Market Revenues & Volume Share, By End-user Industry, 2021 & 2031F |

4 Indonesia Urea Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing demand for urea-based fertilizers due to the growing agriculture sector in Indonesia |

4.2.2 Government initiatives to promote the use of fertilizers to improve crop yield |

4.2.3 Favorable climatic conditions for agriculture leading to higher fertilizer consumption |

4.3 Market Restraints |

4.3.1 Price fluctuations of raw materials impacting the production cost of urea |

4.3.2 Competition from alternative fertilizers like organic fertilizers |

4.3.3 Environmental concerns related to excessive use of chemical fertilizers |

5 Indonesia Urea Market Trends |

6 Indonesia Urea Market, By Types |

6.1 Indonesia Urea Market, By Grade |

6.1.1 Overview and Analysis |

6.1.2 Indonesia Urea Market Revenues & Volume, By Grade, 2021-2031F |

6.1.3 Indonesia Urea Market Revenues & Volume, By Fertilizer, 2021-2031F |

6.1.4 Indonesia Urea Market Revenues & Volume, By Feed, 2021-2031F |

6.1.5 Indonesia Urea Market Revenues & Volume, By Technical, 2021-2031F |

6.2 Indonesia Urea Market, By End-user Industry |

6.2.1 Overview and Analysis |

6.2.2 Indonesia Urea Market Revenues & Volume, By Agriculture, 2021-2031F |

6.2.3 Indonesia Urea Market Revenues & Volume, By Chemical, 2021-2031F |

6.2.4 Indonesia Urea Market Revenues & Volume, By Automotive, 2021-2031F |

6.2.5 Indonesia Urea Market Revenues & Volume, By Medical, 2021-2031F |

6.2.6 Indonesia Urea Market Revenues & Volume, By Others, 2021-2031F |

7 Indonesia Urea Market Import-Export Trade Statistics |

7.1 Indonesia Urea Market Export to Major Countries |

7.2 Indonesia Urea Market Imports from Major Countries |

8 Indonesia Urea Market Key Performance Indicators |

8.1 Average selling price of urea in the market |

8.2 Adoption rate of urea-based fertilizers by farmers |

8.3 Number of government subsidies or incentives promoting the use of urea |

9 Indonesia Urea Market - Opportunity Assessment |

9.1 Indonesia Urea Market Opportunity Assessment, By Grade, 2021 & 2031F |

9.2 Indonesia Urea Market Opportunity Assessment, By End-user Industry, 2021 & 2031F |

10 Indonesia Urea Market - Competitive Landscape |

10.1 Indonesia Urea Market Revenue Share, By Companies, 2024 |

10.2 Indonesia Urea Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Related Reports

- India Switchgear Market Outlook (2026 - 2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

- Saudi Arabia Car Window Tinting Film, Paint Protection Film (PPF), and Ceramic Coating Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- South Africa Stationery Market (2025-2031) | Share, Size, Industry, Value, Growth, Revenue, Analysis, Trends, Segmentation & Outlook

- Afghanistan Rocking Chairs And Adirondack Chairs Market (2026-2032) | Size & Revenue, Competitive Landscape, Share, Segmentation, Industry, Value, Outlook, Analysis, Trends, Growth, Forecast, Companies

- Afghanistan Apparel Market (2026-2032) | Growth, Outlook, Industry, Segmentation, Forecast, Size, Companies, Trends, Value, Share, Analysis & Revenue

Industry Events and Analyst Meet

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Stationery & Paper Expo Saudi Arabia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero