Singapore Coal Market (2024-2030) | Revenue, Companies, Forecast, Industry, Trends, Analysis, Value, Growth, Size, Share & Outlook

Market Forecast By Types (Bituminous Coal, Sub-Bituminous Coal, Anthracite, Lignite), By End-Users (Electricity, Steel, Cement, Others) And Competitive Landscape

| Product Code: ETC038168 | Publication Date: Jul 2023 | Updated Date: Feb 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

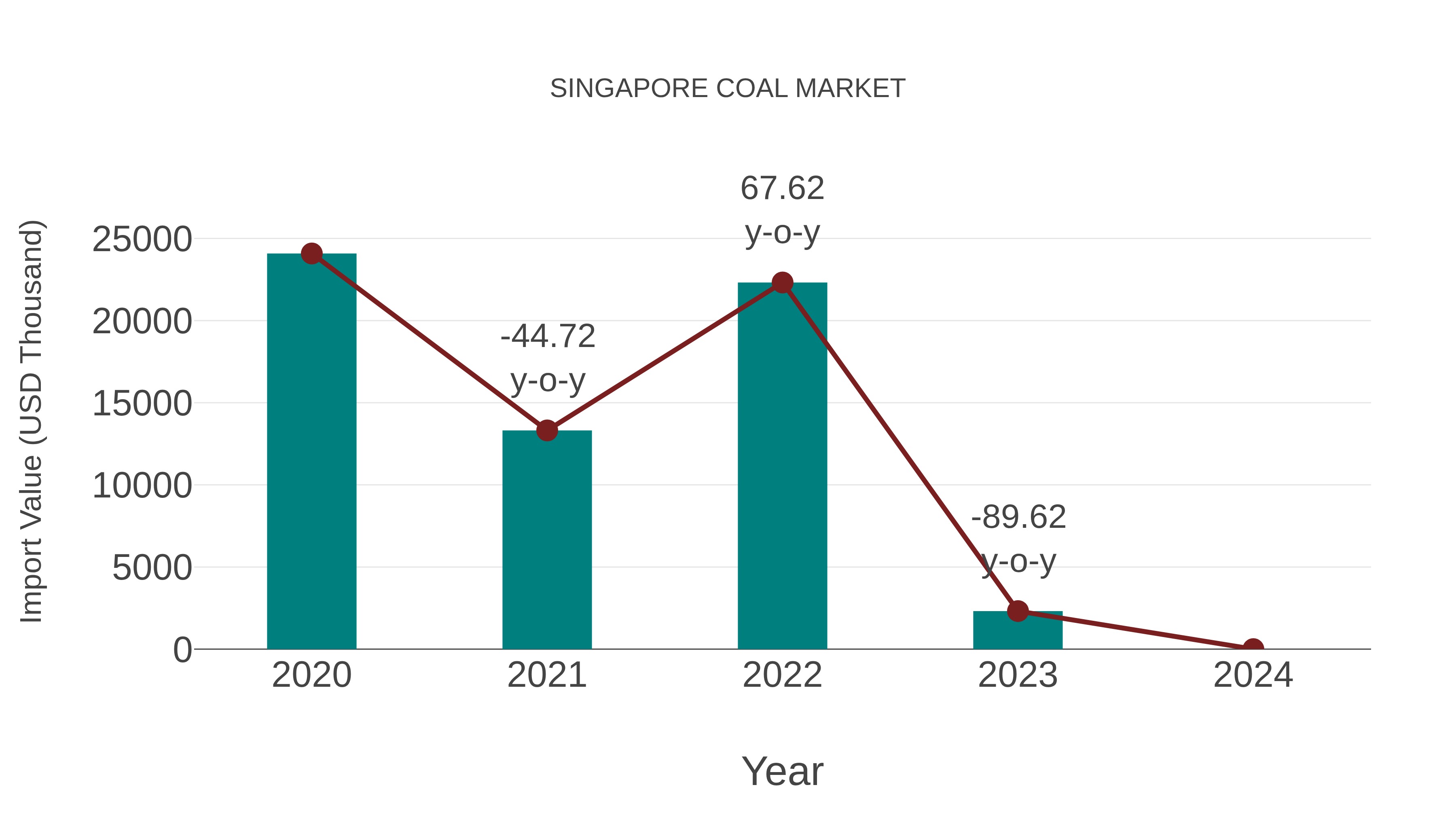

Singapore Coal Market: Import Trend Analysis

In the Singapore coal market, the import trend experienced a notable decline with a Compound Annual Growth Rate (CAGR) of -54.18% during 2020-2024. This sharp decrease suggests a significant shift in demand dynamics or market conditions affecting trade performance.

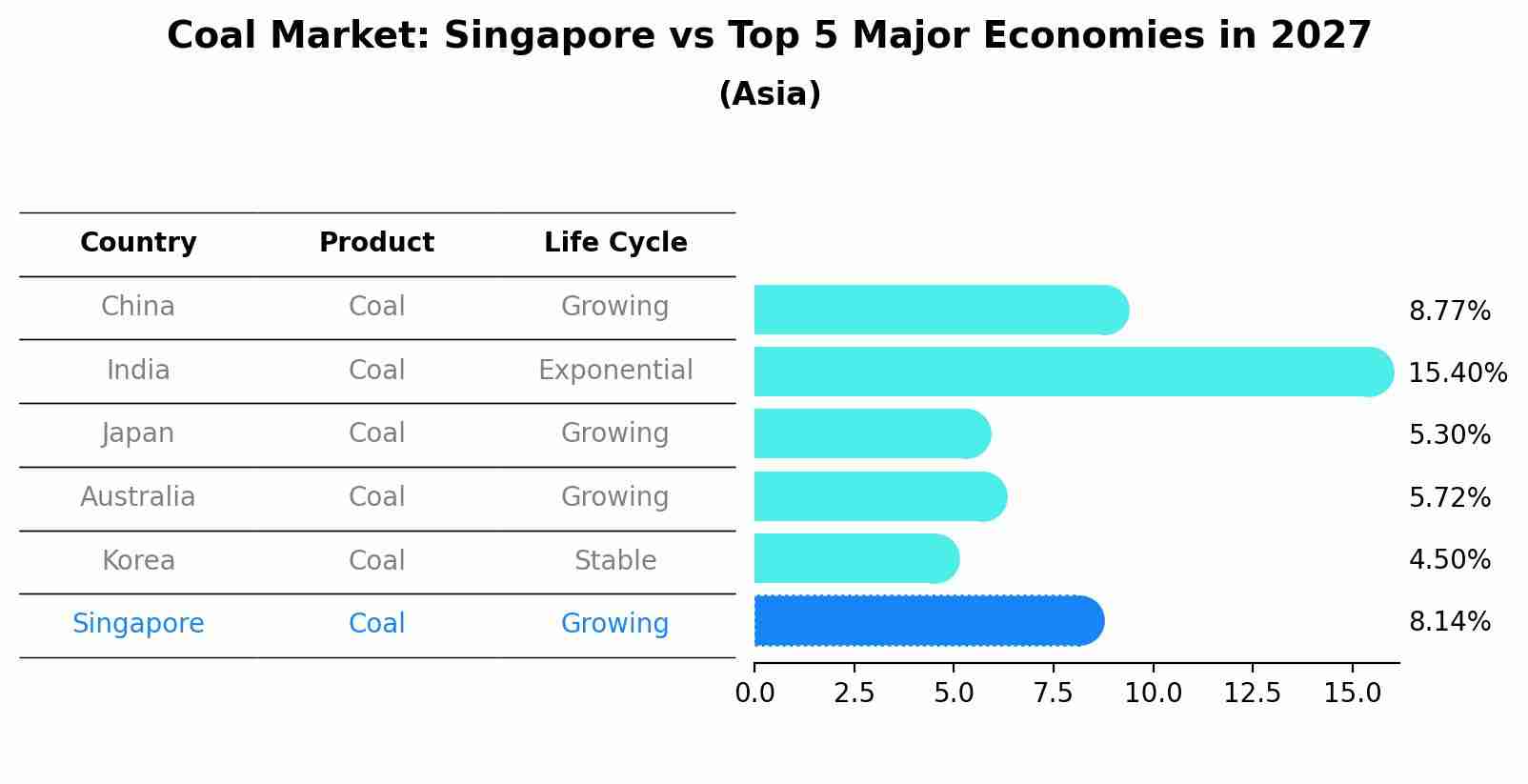

Coal Market: Singapore vs Top 5 Major Economies in 2027 (Asia)

The Coal market in Singapore is projected to grow at a growing growth rate of 8.14% by 2027, highlighting the country's increasing focus on advanced technologies within the Asia region, where China holds the dominant position, followed closely by India, Japan, Australia and South Korea, shaping overall regional demand.

Singapore Coal Market Synopsis

Singapore is the leading oil and gas hub in southeast Asia. It is also a major importer of coal, with imports reaching 8.6 million tonnes in 2019. The Singapore government has taken steps to reduce its reliance on imported coal, however, due to the country`s limited natural resources and lack of domestic production facilities. This makes it increasingly dependent on foreign sources for its energy needs. In 2020, an estimated 9 million tonnes of coal were imported into Singapore primarily from Indonesia and South Africa.

Market Drivers

The main drivers behind the growth of Singapore coal market are increasing demand from utilities and independent power producers (IPPs). As electricity consumption continues to rise across Southeast Asia due to population growth and economic development, more power plants are being built along with increased investments in renewable energy projects such as wind farms and solar parks that will require significant amounts of coal-fired generation capacity to balance out intermittent or variable sources like wind or solar power. Additionally, industrialization has led to a greater need for steel production which relies heavily on metallurgical grade coals found mostly in Indonesia or Russia.

Market challenges

Despite these favourable conditions for the industry there remain several challenges facing the sector including environmental concerns over air pollution associated with burning fossil fuels as well as competition from renewable energy forms like hydroelectricity which can often be produced at lower costs than traditional thermal sources such as coal fired power plants.Furthermore despite having some indigenous reserves most countries have difficulty accessing them due to infrastructure constraints making imports much more preferable option particularly when considering quality concerns regarding certain grades or types of coals mined domestically.Finally there remains political tension between exporters like Australia China Indonesia South Africa ETC who all compete fiercely over pricing availability sustainability credentials ETC

Key players

The major players operating within Singapore Coal Market include PT Adaro Energy Tbk (Indonesia) Rio Tinto Ltd (Australia) BHP Billiton plc (United Kingdom)

Covid-19 Impact

Due to COVID-19 related lockdowns impacting supply chains around the world, prices continued their downward trend seen since late 2018/early 2019 falling by around 10 % year on year throughout 2020.However despite this overall decline many individual markets saw spikes during various points throughout last year driven mainly by sporadic disruptions caused by port closures travel restrictions movement control orders ETC affecting key trading routes particularly those passing through India one of Southeast Asian regions largest traders

Key Highlights of the Report:

- Singapore Coal Market Outlook

- Market Size of Singapore Coal Market, 2023

- Forecast of Singapore Coal Market, 2030

- Historical Data and Forecast of Singapore Coal Revenues & Volume for the Period 2020-2030

- Singapore Coal Market Trend Evolution

- Singapore Coal Market Drivers and Challenges

- Singapore Coal Price Trends

- Singapore Coal Porter's Five Forces

- Singapore Coal Industry Life Cycle

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Types for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Bituminous Coal for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Sub-Bituminous Coal for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Anthracite for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Lignite for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By End-Users for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Electricity for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Steel for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Cement for the Period 2020-2030

- Historical Data and Forecast of Singapore Coal Market Revenues & Volume By Others for the Period 2020-2030

- Singapore Coal Import Export Trade Statistics

- Market Opportunity Assessment By Types

- Market Opportunity Assessment By End-Users

- Singapore Coal Top Companies Market Share

- Singapore Coal Competitive Benchmarking By Technical and Operational Parameters

- Singapore Coal Company Profiles

- Singapore Coal Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Singapore Coal Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Singapore Coal Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Singapore Coal Market Overview |

3.1 Singapore Country Macro Economic Indicators |

3.2 Singapore Coal Market Revenues & Volume, 2020 & 2030F |

3.3 Singapore Coal Market - Industry Life Cycle |

3.4 Singapore Coal Market - Porter's Five Forces |

3.5 Singapore Coal Market Revenues & Volume Share, By Types, 2020 & 2030F |

3.6 Singapore Coal Market Revenues & Volume Share, By End-Users, 2020 & 2030F |

4 Singapore Coal Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.3 Market Restraints |

5 Singapore Coal Market Trends |

6 Singapore Coal Market, By Types |

6.1 Singapore Coal Market, By Types |

6.1.1 Overview and Analysis |

6.1.2 Singapore Coal Market Revenues & Volume, By Types, 2020-2030F |

6.1.3 Singapore Coal Market Revenues & Volume, By Bituminous Coal, 2020-2030F |

6.1.4 Singapore Coal Market Revenues & Volume, By Sub-Bituminous Coal, 2020-2030F |

6.1.5 Singapore Coal Market Revenues & Volume, By Anthracite, 2020-2030F |

6.1.6 Singapore Coal Market Revenues & Volume, By Lignite, 2020-2030F |

6.2 Singapore Coal Market, By End-Users |

6.2.1 Overview and Analysis |

6.2.2 Singapore Coal Market Revenues & Volume, By Electricity, 2020-2030F |

6.2.3 Singapore Coal Market Revenues & Volume, By Steel, 2020-2030F |

6.2.4 Singapore Coal Market Revenues & Volume, By Cement, 2020-2030F |

6.2.5 Singapore Coal Market Revenues & Volume, By Others, 2020-2030F |

7 Singapore Coal Market Import-Export Trade Statistics |

7.1 Singapore Coal Market Export to Major Countries |

7.2 Singapore Coal Market Imports from Major Countries |

8 Singapore Coal Market Key Performance Indicators |

9 Singapore Coal Market - Opportunity Assessment |

9.1 Singapore Coal Market Opportunity Assessment, By Types, 2020 & 2030F |

9.2 Singapore Coal Market Opportunity Assessment, By End-Users, 2020 & 2030F |

10 Singapore Coal Market - Competitive Landscape |

10.1 Singapore Coal Market Revenue Share, By Companies, 2023 |

10.2 Singapore Coal Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Taiwan Food Delivery Platform Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026-2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero