China Smart TV Market (2025-2031) | Industry, Revenue, Analysis, Trends, Growth, Share, Outlook, Size, Companies, Forecast & Value

Market Forecast By Screen Type (28 to 40 inch, 41 to 59 inch, 60 inch & above), By Pannel Type (LED, OLED, QLED, Others), By Resolution Type (HD TV, Full HD TV, 4K UHD TV, 8K TV), By Distribution Channel (Direct, Indirect), By End Use (Commercial, Residential, Others) And Competitive Landscape

| Product Code: ETC012221 | Publication Date: Oct 2020 | Updated Date: Oct 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

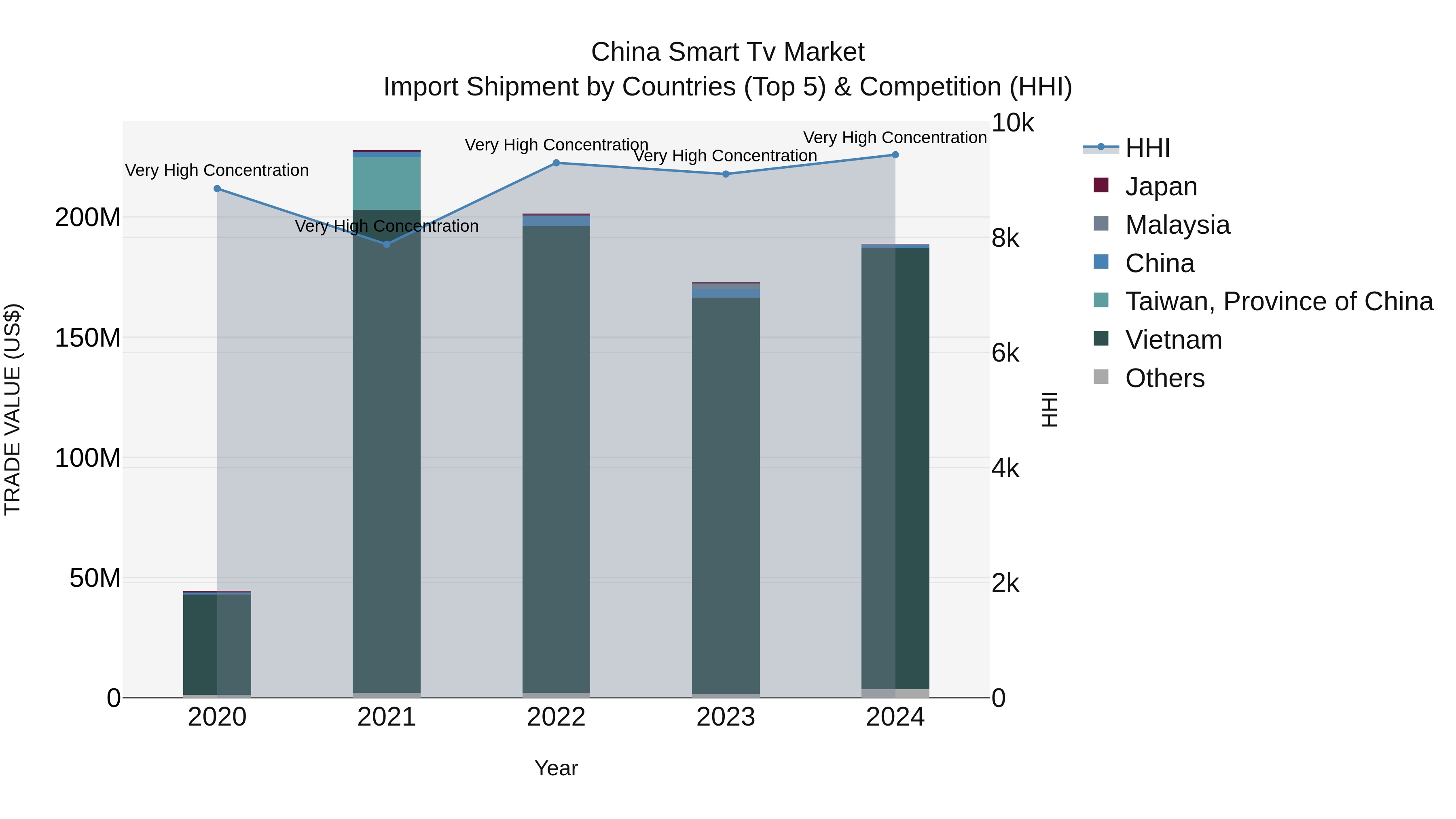

China Smart Tv Market Top 5 Importing Countries and Market Competition (HHI) Analysis

In 2024, China continued to see a significant influx of smart TV imports, with Vietnam, Indonesia, and Malaysia emerging as key exporting countries alongside Metropolitan France. The high Herfindahl-Hirschman Index (HHI) indicates a concentrated market, highlighting the dominance of these top exporters. A remarkable Compound Annual Growth Rate (CAGR) of 43.55% from 2020 to 2024 underlines the robust expansion of the smart TV import market in China. Furthermore, the growth rate of 9.25% from 2023 to 2024 demonstrates sustained momentum, pointing towards continued opportunities and demand in the sector.

China Smart TV Market Highlights

| Report Name | China Smart TV Market |

| Forecast period | 2025-2031 |

| CAGR | 7.5% |

| Growing Sector | Media & Entertainment Sector |

Topics Covered in the China Smart TV Market Report

China Smart TV Market report thoroughly covers the market by Screen Types, by Panel Types, by Resolution Types, by Distribution Channels and by End use. The market report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high growth areas, and market drivers which would help the stakeholders to devise and align their market strategies according to the current and future market dynamics.

China Smart TV Market Synopsis

The China Smart TV market has experienced rapid growth over the past few years. The technology advancements and increasing preference for specialized entertainment devices is driving the market. As urbanization increases and demand of innovative devices likely to increase because the people likely to invest in products containing special features. According to market research, smart TV sales reached Chinese households over 70% end of the 2022. And 4K and OLED displays played a major role to reach 60% of production in 2021.

Features such as built-in AI, voice assistance, and streaming services, smart TVs have boosted sales. The expanding middle class and the growing popularity of streaming platforms, such as IQIYI and Tencent Video, have also fuelled this trend. Further, the rise of affordable smart TV options and the expansion of internet infrastructure in rural areas have further fuelled the market’s growth. With annual sales exceeding 49 million units in 2024, the smart tv market continues to boos in the future.

According to 6Wresearch, the China Smart TV Market is anticipated to grow at a CAGR of 7.5% during the forecast period 2025-2031. The China smart TV market has been experiencing significant growth. The market is driven by advancements in technology and increasing consumer demand for high-quality entertainment experiences. The integration of artificial intelligence (AI), 4K and 8K resolutions, and interactive features has made smart TVs increasingly appealing to consumers. Furthermore, due to intense competition we get the products at affordable price. While the growing adoption of internet-connected devices are also responsible for the market expansion. Nowadays, the smart tv became the central hub for home entertainment, as Over-the-top OTT platform has emerged.

Despite the growth, the China smart TV market faces several challenges. The profit margin is reduced for manufacturers, requiring constant innovation to maintain a competitive edge. Additionally, some reports have revealed about high-profile case of data breaches and unauthorised data sharing those alarming concerns among consumers and creating trust issues. Sometimes economic fluctuations and supply chain disruptions, particularly in the semiconductor industry, also pose hurdles that can impact production and pricing. Overcoming these challenges is crucial for sustainable growth in the China smart TV market.

China Smart TV Market Trends

The China Smart TV market is witnessing rapid growth driven by advancements in technology, increasing internet penetration, and the rising demand for connected home entertainment systems. With more consumers seeking seamless streaming experiences, features like AI-powered voice assistants, 4K and 8K resolution displays, and customizable interfaces are becoming key differentiators among brands. Domestic players such as Xiaomi, Hisense, and TCL dominate the market with competitively priced models and innovative features tailored to local preferences, while global brands continue to expand their presence. The shift towards OTT platforms and integration with IoT devices further propels the market, positioning Smart TVs as central hubs in smart home ecosystems.

Investment Opportunities in the China Smart TV Market

The China Smart TV market presents significant investment opportunities due to its rapid technological advancements and growing consumer demand for connected devices. With an increasing middle-class population and rising internet penetration, there is a surge in demand for smart home entertainment systems. Leading manufacturers and new entrants are focusing on integrating AI, voice recognition, and IoT capabilities into smart TVs, making them an integral part of the evolving smart home ecosystem. Additionally, China's government policies promoting digital innovation and domestic manufacturing bolster the market's growth potential. Investors can capitalize on this trend by supporting companies that prioritize innovation, localized content integration, and competitive pricing strategies.

Leading Players in the China Smart TV Market

The China smart TV market is dominated by several key players that have significantly influenced the industry with their innovative technologies and competitive strategies. Companies like Xiaomi, Huawei, and TCL have established themselves as leaders due to their diverse product offerings, cutting-edge designs, and integration of advanced features such as AI and IoT capabilities. Xiaomi, for instance, has gained popularity with its affordable and feature-rich smart TVs catering to a wide customer base. TCL, a global brand headquartered in China, is known for its high-quality displays and competitive pricing. Meanwhile, Huawei has made strides with its smart TVs by leveraging its ecosystem of interconnected devices to enhance user experiences. These brands, among others, continue to shape and define the dynamic landscape of the smart TV market in China.

Government Regulations

The government regulations on the China smart TV market mainly focus on ensuring content compliance, data security, and fair competition. Authorities mandate that smart TV manufacturers adhere to strict content guidelines to prevent unauthorized or harmful materials from being displayed. Additionally, regulations emphasize the importance of protecting user data and privacy, requiring companies to implement robust data security measures and transparency in data usage. To foster fair competition, the government monitors market behavior, aiming to prevent monopolistic practices and promote innovation within the industry. These measures collectively aim to maintain a healthy, secure, and competitive smart TV market in China.

Future Insights of the China Smart TV Market

The China Smart TV market is poised for significant growth in the coming years, driven by advancements in AI technology, the integration of Internet of Things (IoT) capabilities, and rising consumer demand for enhanced viewing experiences. As content streaming platforms expand and 5G technology becomes more widespread, smart TVs are expected to become central hubs for connected ecosystems within households. Additionally, with increasing competition among manufacturers, features such as personalized recommendations, voice recognition, and ultra-high-definition displays are likely to become standard. This evolution positions the China Smart TV market as a key player in shaping global trends in home entertainment technology.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Smart TVs to Dominate the Market - By Screen Type

According to Vasu, Senior Research Analyst, 6Wresearch, it is analyzed that the China Smart TV market is expected to witness steady growth, with 41 to 59-inch screens leading the product segment. This dominance is driven by their popularity among residential users, offering the perfect balance between screen size and affordability. Larger screens, particularly 60 inches and above, are increasingly in demand in commercial spaces and luxury residential markets. Smaller screens (28 to 40 inches) continue to appeal to budget-conscious households and those with limited space.

LED Panels to Dominate the Market - By Panel Type

It is observed that LED panels are set to dominate the China Smart TV market. The cost-effectiveness of LED has made it popular among consumers. OLED and QLED panels are gaining traction, particularly among high-income consumers, for their superior visual quality and premium appeal. Other panel types remain niche, with minimal adoption across the market.

4K UHD TVs to Dominate the Market - By Resolution Type

It is observed that 4K UHD TVs are expected to drive significant growth in China, due to their increasing affordability and the rising demand for premium-quality viewing experiences. Full HD TVs continue to perform well in the budget and mid-range segments, while HD TVs are experiencing a steady decline in popularity. At the same time, 8K TVs are emerging as a high-end option for affluent and tech-savvy buyers, though adoption remains limited at this stage.

Indirect Channels to Dominate the Market - By Distribution Channel

It is observed that indirect distribution channels, including retail stores and e-commerce platforms, are expected to dominate the China Smart TV market. For high-value purchases, physical stores are preferred by consumers who value in-person guidance and hands-on product demonstrations. Meanwhile, e-commerce platforms are rapidly gaining traction, driven by widespread internet access, aggressive pricing strategies, and the convenience of home delivery services.

Residential Segment to Dominate the Market - By End Use

It is observed that the residential segment is expected to lead the China Smart TV market, with growing interest in advanced smart home entertainment systems. Commercial use, such as in hotels and corporate setups, is also on the rise, primarily favoring larger-screen televisions. Other niche applications continue to hold a smaller but stable share of the market, catering to specialized needs.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024

- Base Year: 2024

- Forecast Data until 2031

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- China Smart TV Market Outlook

- Market Size of China Smart TV Market, 2024

- Forecast of China Smart TV Market, 2031

- Historical Data and Forecast of China Smart TV Revenues & Volume for the Period 2021 - 2031

- China Smart TV Market Trend Evolution

- China Smart TV Market Drivers and Challenges

- China Smart TV Price Trends

- China Smart TV Porter's Five Forces

- China Smart TV Industry Life Cycle

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Screen Type for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By 28 to 40 inch for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By 41 to 59 inch for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By 60 inch & above for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Pannel Type for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By LED for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By OLED for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By QLED for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Others for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Resolution Type for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By HD TV for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Full HD TV for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By 4K UHD TV for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By 8K TV for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Distribution Channel for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Direct for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Indirect for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By End Use for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Commercial for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Residential for the Period 2021 - 2031

- Historical Data and Forecast of China Smart TV Market Revenues & Volume By Others for the Period 2021 - 2031

- China Smart TV Import Export Trade Statistics

- Market Opportunity Assessment By Screen Type

- Market Opportunity Assessment By Panel Type

- Market Opportunity Assessment By Resolution Type

- Market Opportunity Assessment By Distribution Channel

- Market Opportunity Assessment By End Use

- China Smart TV Top Companies Market Share

- China Smart TV Competitive Benchmarking By Technical and Operational Parameters

- China Smart TV Company Profiles

- China Smart TV Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments and their leading categories:

By Screen Type

- 28 To 40 Inch

- 41 To 59 Inch

- 60 Inch & Above

By Panel Type

- LED

- OLED

- QLED

- Others

By Resolution Type

- HD TV

- Full HD TV

- 4K UHD TV

- 8K TV

By Distribution Channel

- Direct

- Indirect

By End Use

- Commercial

- Residential

- Others

China Smart TV Market (2025-2031): FAQs

The smart TV market in China has seen consistent growth due to advancements in technology, increasing demand for high-quality home entertainment systems, and the rise of internet connectivity across the country.

Major players in the China smart TV market include Xiaomi, Hisense, TCL, and Skyworth, all of which compete by offering innovative features and affordable options.

Key factors include the expansion of 4K and 8K technology, integration of AI and voice control, and the growing availability of streaming platforms that cater to a wide audience.

Consumers in China are increasingly seeking larger screens, enhanced audio-visual experiences, and seamless connectivity with other smart devices, which has significantly shaped market offerings and innovation.

6Wresearch actively monitors the China Smart TV Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Smart TV Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Smart TV Market Overview |

| 3.1 China Smart TV Market Revenues & Volume, 2021 - 2031F |

| 3.2 China Smart TV Market - Industry Life Cycle |

| 3.3 China Smart TV Market - Porter's Five Forces |

| 3.4 China Smart TV Market Revenues & Volume Share, By Screen Type, 2021 & 2031F |

| 3.5 China Smart TV Market Revenues & Volume Share, By Pannel Type, 2021 & 2031F |

| 3.6 China Smart TV Market Revenues & Volume Share, By Resolution Type, 2021 & 2031F |

| 3.7 China Smart TV Market Revenues & Volume Share, By Distribution Channel, 2021 & 2031F |

| 3.8 China Smart TV Market Revenues & Volume Share, By End Use, 2021 & 2031F |

| 4 China Smart TV Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income and urbanization in China leading to higher demand for smart TVs. |

| 4.2.2 Technological advancements and innovation in smart TV features and functionalities. |

| 4.2.3 Growing popularity of online streaming services and content consumption driving the adoption of smart TVs. |

| 4.3 Market Restraints |

| 4.3.1 High initial cost of smart TVs compared to traditional TVs impacting adoption rates. |

| 4.3.2 Concerns regarding data privacy and security in smart TVs hindering consumer trust and adoption. |

| 4.3.3 Intense competition among smart TV manufacturers leading to pricing pressures and margin challenges. |

| 5 China Smart TV Market Trends |

| 6 China Smart TV Market Segmentation |

| 6.1 China Smart TV Market, By Screen Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Smart TV Market Revenues & Volume, By Screen Type, 2021 - 2031F |

| 6.1.3 China Smart TV Market Revenues & Volume, By 28 to 40 inch, 2021 - 2031F |

| 6.1.4 China Smart TV Market Revenues & Volume, By 41 to 59 inch, 2021 - 2031F |

| 6.1.5 China Smart TV Market Revenues & Volume, By 60 inch & above, 2021 - 2031F |

| 6.2 China Smart TV Market, By Pannel Type |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Smart TV Market Revenues & Volume, By LED, 2021 - 2031F |

| 6.2.3 China Smart TV Market Revenues & Volume, By OLED, 2021 - 2031F |

| 6.2.4 China Smart TV Market Revenues & Volume, By QLED, 2021 - 2031F |

| 6.2.5 China Smart TV Market Revenues & Volume, By Others, 2021 - 2031F |

| 6.3 China Smart TV Market, By Resolution Type |

| 6.3.1 Overview and Analysis |

| 6.3.2 China Smart TV Market Revenues & Volume, By HD TV, 2021 - 2031F |

| 6.3.3 China Smart TV Market Revenues & Volume, By Full HD TV, 2021 - 2031F |

| 6.3.4 China Smart TV Market Revenues & Volume, By 4K UHD TV, 2021 - 2031F |

| 6.3.5 China Smart TV Market Revenues & Volume, By 8K TV, 2021 - 2031F |

| 6.4 China Smart TV Market, By Distribution Channel |

| 6.4.1 Overview and Analysis |

| 6.4.2 China Smart TV Market Revenues & Volume, By Direct, 2021 - 2031F |

| 6.4.3 China Smart TV Market Revenues & Volume, By Indirect, 2021 - 2031F |

| 6.5 China Smart TV Market, By End Use |

| 6.5.1 Overview and Analysis |

| 6.5.2 China Smart TV Market Revenues & Volume, By Commercial, 2021 - 2031F |

| 6.5.3 China Smart TV Market Revenues & Volume, By Residential, 2021 - 2031F |

| 6.5.4 China Smart TV Market Revenues & Volume, By Others, 2021 - 2031F |

| 7 China Smart TV Market Import-Export Trade Statistics |

| 7.1 China Smart TV Market Export to Major Countries |

| 7.2 China Smart TV Market Imports from Major Countries |

| 8 China Smart TV Market Key Performance Indicators |

| 8.1 Average time spent on smart TV apps per user. |

| 8.2 Percentage of households with internet connectivity opting for smart TVs. |

| 8.3 Customer satisfaction score with smart TV user experience. |

| 8.4 Number of new smart TV features or technologies introduced annually. |

| 8.5 Percentage of smart TV users utilizing voice control or AI features. |

| 9 China Smart TV Market - Opportunity Assessment |

| 9.1 China Smart TV Market Opportunity Assessment, By Screen Type, 2021 & 2031F |

| 9.2 China Smart TV Market Opportunity Assessment, By Pannel Type, 2021 & 2031F |

| 9.3 China Smart TV Market Opportunity Assessment, By Resolution Type, 2021 & 2031F |

| 9.4 China Smart TV Market Opportunity Assessment, By Distribution Channel, 2021 & 2031F |

| 9.5 China Smart TV Market Opportunity Assessment, By End Use, 2021 & 2031F |

| 10 China Smart TV Market - Competitive Landscape |

| 10.1 China Smart TV Market Revenue Share, By Companies, 2024 |

| 10.2 China Smart TV Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Qatar Access and Home Network Market (2026-2032)

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.