India Sugar Market (2025-2031) | Size, Industry, Value, Trends, Revenue, Share, Analysis, Growth, Outlook, Companies & Forecast

Market Forecast By Types (White Sugar, Brown Sugar, Liquid Sugar), By Form (Granulated Sugar, Powdered Sugar, Syrup Sugar), By End -Users (Food and Beverages, Pharma and Personal Care, Household), By Sources (Sugarcane, Sugarbeet) And Competitive Landscape

| Product Code: ETC045424 | Publication Date: Aug 2023 | Updated Date: Nov 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

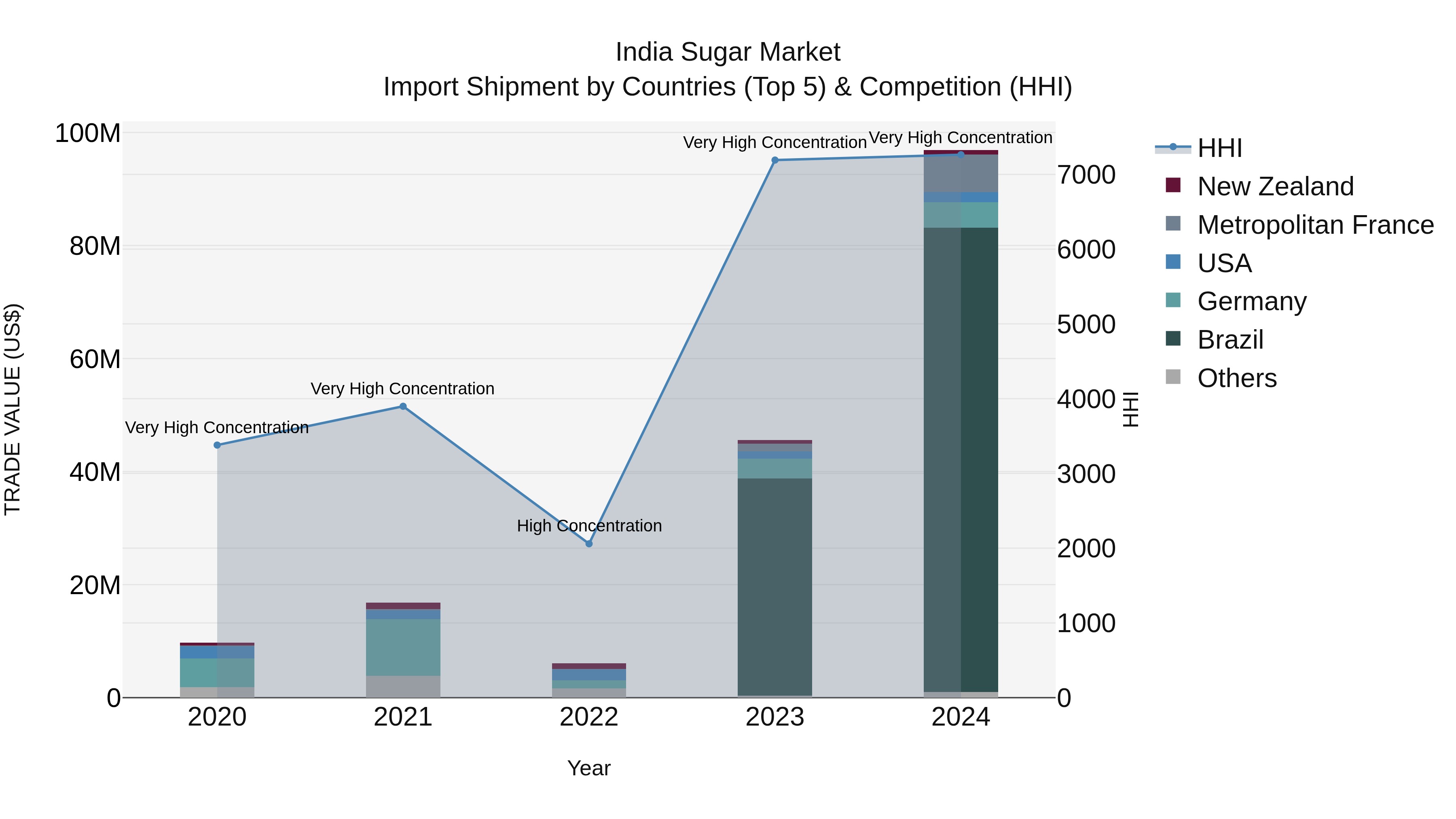

India Sugar Market Top 5 Importing Countries and Market Competition (HHI) Analysis

India`s sugar import market in 2024 saw significant contributions from top exporting countries like Brazil, Metropolitan France, Germany, USA, and New Zealand. The Herfindahl-Hirschman Index (HHI) indicated a high concentration within the market. The impressive compound annual growth rate (CAGR) of 77.54% from 2020 to 2024 showcases the increasing demand for sugar imports in India. Moreover, the remarkable growth rate of 112.62% from 2023 to 2024 highlights a rapid acceleration in import volumes, reflecting the evolving dynamics of the industry.

India Sugar Market Highlights

| Report Name | India Sugar Market |

| Forecast Period | 2025-2031 |

| CAGR | 5.4% |

| Growing Sector | Agricultural and Food Processing |

Topics Covered in the India Sugar Market Report

The India Sugar Market report thoroughly covers the market by Types, Form, End -Users and Sources. The market report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high growth areas, and market drivers, which would help the stakeholders devise and align their market strategies according to the current and future market dynamics.

India Sugar Market Synopsis

The India Sugar Industry is a vital component of the country's economic framework. It creates a strong link between agriculture and industrial production, promoting rural development through job creation. The industry also supports several related sectors, including food processing, bioenergy, and pharmaceuticals. Additionally, it benefits from robust domestic demand and the growing focus on sustainability, particularly in the production of sugarcane ethanol. This shift towards advanced processing techniques emphasizes sustainability and continues to significantly contribute to the agro-industrial growth of India.

According to 6Wresearch, the India Sugar Market is estimated to reach a CAGR of 5.4% during the forecast period 2025-2031. Several factors drive growth in the Indian sugar industry, including the rise in per capita income, changing consumption patterns due to increased urbanization, and government policies that promote ethanol blending to reduce reliance on fossil fuels. Additionally, technological advancements in farming and sugar processing have contributed to greater efficiency and higher yields in the India sugar market size. Export growth plays a vital role as Indian sugar is now recognized for its improved quality standards in global markets.

However, the industry faces numerous challenges. Inconsistent rainfall and climate-induced disruptions impact sugarcane yields and overall production output. The water-intensive nature of sugar production places further stress on already limited resources, particularly in drought-prone areas. There is also a need for substantial investment in green technologies to ensure environmental sustainability and reduce carbon emissions. Additionally, constant fluctuations in the international sugar market create uncertainty for stakeholders. Despite these challenges, the industry is rapidly evolving to address these issues, helping it maintain a significant part of the India Sugar Market share and ensuring its important role in global sugar production in the coming years.

India Sugar Market Trends

The India sugar market is experiencing notable shifts and developments shaping its trajectory. Below are the key trends driving the industry:

- Technological Advancements: The adoption of automation and innovative farming techniques is accelerating efficiency in sugarcane cultivation and processing.

- Government Policies: Supportive policies, including subsidies and export incentives, are fostering the India Sugar Market growth by bolstering domestic production and global competitiveness.

- Shift Towards Sustainability: A focus on eco-friendly farming practices and renewable energy use in production processes is addressing environmental concerns.

- Ethanol Blending Initiative: The growing emphasis on ethanol production from sugarcane is diversifying revenue streams, contributing positively to the India Sugar Market revenue.

- Global Trade Opportunities: Increasing demand for Indian sugar in international markets highlights its competitive quality and price positioning.

These trends underline the dynamic landscape of the India sugar market, reflecting its resilience and adaptability to emerging challenges and global demand shifts.

Investment Opportunities in the India Sugar Market

India Sugar Market continues to exhibit significant growth potential, driven by evolving consumption patterns, innovation, and global trade dynamics. With expanding domestic and international demand, strategic investments can yield substantial returns. Key opportunities include:

- Ethanol Production Expansion: Increased government support for ethanol blending creates lucrative prospects for producers to diversify and enhance revenues.

- Adoption of Smart Technologies: Investing in AI-driven agriculture and automation tools can optimize production efficiency and reduce costs in sugarcane farming and processing.

- Export Growth Potential: Rising global demand for Indian sugar offers untapped opportunities for businesses to strengthen their presence in international markets, improving India Sugar Market share.

- Renewable Energy Projects: Utilizing sugar industry by-products like bagasse for power generation contributes to sustainability while unlocking additional revenue avenues.

- Value-Added Products: The growing interest in speciality and health-focused sugar products, such as organic or low-glycemic options, provides opportunities to target niche markets.

These investment approaches, aligned with market trends, offer pathways for enhancing competitiveness and realizing long-term growth within the India Sugar Market.

Leading Players in the India Sugar Market

India Sugar Market is supported by several key players who contribute significantly to its growth and innovation. These companies invest in advanced technologies and sustainable practices to maintain their competitive edge and maximize India Sugar Market revenue.

- Bajaj Hindusthan Sugar Ltd: A prominent name in the sector, the company is known for its extensive production capacity and focused diversification into ethanol and power generation.

- Balrampur Chini Mills Ltd: Renowned for its efficient operations, the company excels in producing quality sugar and value-added products like ethanol.

- Shree Renuka Sugars Ltd: A major contributor with a robust global footprint, focusing on renewable energy and expanding its product portfolio.

- Triveni Engineering & Industries Ltd: Apart from sugar production, the company leverages innovations in co-products like power and distillery to drive revenue growth.

These companies play a pivotal role in bolstering the market's resilience, ensuring sustainable growth, and meeting diverse consumer demands. Their strategies continue to shape a dynamic and thriving future for the India Sugar Market.

Government Regulations of The Report

The regulations governing the sugar industry in India, maintained by the government, are complex and aim to balance competing interests with long-term development. They address various issues, including sugarcane procurement, production standards, and market interventions. To ensure that farmers receive fair returns while supporting operational needs, the government has established a pricing regime.

Additionally, to facilitate diversification and reduce surplus pressure on the domestic market, the government provides incentives, such as the production and use of ethanol derived from sugarcane. Import and export policies are carefully designed to counterbalance the unpredictable nature of global markets. At the same time, these regulations encourage efficiency, sustained development, and the adoption of technological advancements throughout the sector. The combination of these typically weak areas presents significant opportunities for improvement, allowing the India sugar industry to enhance its competitiveness in an ever-changing economic and environmental landscape.

Future Insights of the India Sugar Market

India Sugar Market size is poised for substantial growth, driven by increasing domestic consumption and rising export opportunities. The sector is moving towards sustainable practices, which will lead to the adoption of innovative technologies that increase efficiency and reduce environmental impact. Government mandates for ethanol blending in fuels will promote increased ethanol production, providing additional revenue and decreasing reliance on traditional outputs. Furthermore, the rising demand for sugar substitutes and value-added products offers another opportunity for diversification among industry players. Urbanization and population growth will continue to drive demand in the food and beverage industries. However, the ability to adapt to climate variability and fluctuations in global prices is crucial. Strategic investments in infrastructure and research will be vital for enhancing future performance in the market.

Market Segmentation Analysis

The Report offers a comprehensive study of the subsequent market segments and their leading categories.

White Sugar to Dominate Market - By Types

White sugar is projected to dominate this segment due to its widespread use across households, food production, and the pharmaceutical industry. Its versatility, longer shelf life, and suitability for a variety of applications make it the preferred choice. White sugar’s standard quality and ease of availability also contribute to its leading position in this segment.

Granulated Sugar to Dominate Market - By Form

Granulated sugar is expected to lead this segment due to its prevalence in both industrial applications and household consumption. Its convenient form and ease of measurement enhance its utility, making it a staple in recipes ranging from baking to beverages. Granulated sugar also offers better shelf stability compared to powdered or syrup forms.

Food and Beverages to Dominate Market - By End-Users

The food and beverages industry is anticipated to remain the largest consumer of sugar in this segment. Its reliance on sugar for large-scale production of sweets, snacks, drinks, and processed goods highlights its critical importance. With evolving consumer preferences for ready-to-eat and indulgent products, this sector’s sugar demand is expected to grow consistently.

Sugarcane to Dominate Market - By Sources

According to Aayushi, Senior Research Analyst, 6Wresearch, sugarcane continues to dominate as the leading source of sugar in India, supported by efficient production systems and high yield rates. Its extensive cultivation across different climatic regions and competitive cost of production makes it a preferred raw material. Better supply chain management for sugarcane also ensures seamless processing and distribution.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024

- Forecast Data until 2031.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- India Sugar Market Outlook

- Market Size of India Sugar Market, 2024

- Forecast of India Sugar Market, 2031

- Historical Data and Forecast of India Sugar Revenues & Volume for the Period 2021-2031

- India Sugar Market Trend Evolution

- India Sugar Market Drivers and Challenges

- India Sugar Price Trends

- India Sugar Porter's Five Forces

- India Sugar Industry Life Cycle

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Types for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By White Sugar for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Brown Sugar for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Liquid Sugar for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Form for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Granulated Sugar for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Powdered Sugar for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Syrup Sugar for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By End -Users for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Food and Beverages for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Pharma and Personal Care for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Household for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Sources for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Sugarcane for the Period 2021-2031

- Historical Data and Forecast of India Sugar Market Revenues & Volume By Sugarbeet for the Period 2021-2031

- India Sugar Import Export Trade Statistics

- Market Opportunity Assessment By Types

- Market Opportunity Assessment By Form

- Market Opportunity Assessment By End -Users

- Market Opportunity Assessment By Sources

- India Sugar Top Companies Market Share

- India Sugar Competitive Benchmarking By Technical and Operational Parameters

- India Sugar Company Profiles

- India Sugar Key Strategic Recommendations

Market Segmentation Analysis

The Report offers a comprehensive study of the subsequent market segments and their leading categories.

By Types

- White Sugar

- Brown Sugar

- Liquid Sugar

By Form

- Granulated Sugar

- Powdered Sugar

- Syrup Sugar

By End -User

- Food and Beverages

- Pharma and Personal Care

- Household

By Sources

- Sugarcane

- Sugarbeet

India Sugar Market (2025-2031): FAQs

Increasing demand in the food and beverages sector, coupled with consistent production of sugarcane, is driving the market's growth.

An efficient sugarcane supply chain ensures steady production, processing, and distribution, supporting market growth.

Sugar acts as a key ingredient in a variety of processed foods and drinks, meeting the preferences of evolving consumers.

The preference for ready-to-eat and indulgent products fuels a consistent demand for sugar in the food sector.

Sugarcane's high yield rates, extensive cultivation, and competitive cost make it the leading source of sugar in India.

6Wresearch actively monitors the India Sugar Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the India Sugar Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 India Sugar Market Overview |

| 3.1 India Country Macro Economic Indicators |

| 3.2 India Sugar Market Revenues & Volume, 2021 & 2031F |

| 3.3 India Sugar Market - Industry Life Cycle |

| 3.4 India Sugar Market - Porter's Five Forces |

| 3.5 India Sugar Market Revenues & Volume Share, By Types, 2021 & 2031F |

| 3.6 India Sugar Market Revenues & Volume Share, By Form, 2021 & 2031F |

| 3.7 India Sugar Market Revenues & Volume Share, By End -Users, 2021 & 2031F |

| 3.8 India Sugar Market Revenues & Volume Share, By Sources, 2021 & 2031F |

| 4 India Sugar Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing demand for packaged and convenience foods in India |

| 4.2.2 Growth in the food processing industry leading to higher sugar consumption |

| 4.2.3 Rising population and disposable income levels driving sugar consumption |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating sugar prices due to factors like weather conditions and government policies |

| 4.3.2 Health concerns and increasing awareness about the negative effects of consuming excessive sugar |

| 4.3.3 Competition from alternative sweeteners impacting sugar market growth |

| 5 India Sugar Market Trends |

| 6 India Sugar Market, By Types |

| 6.1 India Sugar Market, By Types |

| 6.1.1 Overview and Analysis |

| 6.1.2 India Sugar Market Revenues & Volume, By Types, 2021-2031F |

| 6.1.3 India Sugar Market Revenues & Volume, By White Sugar, 2021-2031F |

| 6.1.4 India Sugar Market Revenues & Volume, By Brown Sugar, 2021-2031F |

| 6.1.5 India Sugar Market Revenues & Volume, By Liquid Sugar, 2021-2031F |

| 6.2 India Sugar Market, By Form |

| 6.2.1 Overview and Analysis |

| 6.2.2 India Sugar Market Revenues & Volume, By Granulated Sugar, 2021-2031F |

| 6.2.3 India Sugar Market Revenues & Volume, By Powdered Sugar, 2021-2031F |

| 6.2.4 India Sugar Market Revenues & Volume, By Syrup Sugar, 2021-2031F |

| 6.3 India Sugar Market, By End -Users |

| 6.3.1 Overview and Analysis |

| 6.3.2 India Sugar Market Revenues & Volume, By Food and Beverages, 2021-2031F |

| 6.3.3 India Sugar Market Revenues & Volume, By Pharma and Personal Care, 2021-2031F |

| 6.3.4 India Sugar Market Revenues & Volume, By Household, 2021-2031F |

| 6.4 India Sugar Market, By Sources |

| 6.4.1 Overview and Analysis |

| 6.4.2 India Sugar Market Revenues & Volume, By Sugarcane, 2021-2031F |

| 6.4.3 India Sugar Market Revenues & Volume, By Sugarbeet, 2021-2031F |

| 7 India Sugar Market Import-Export Trade Statistics |

| 7.1 India Sugar Market Export to Major Countries |

| 7.2 India Sugar Market Imports from Major Countries |

| 8 India Sugar Market Key Performance Indicators |

| 8.1 Average per capita sugar consumption in India |

| 8.2 Growth rate of the food processing industry in India |

| 8.3 Import and export trends of sugar in India |

| 8.4 Adoption rate of alternative sweeteners in the market |

| 8.5 Investment trends in the sugar industry in India |

| 9 India Sugar Market - Opportunity Assessment |

| 9.1 India Sugar Market Opportunity Assessment, By Types, 2021 & 2031F |

| 9.2 India Sugar Market Opportunity Assessment, By Form, 2021 & 2031F |

| 9.3 India Sugar Market Opportunity Assessment, By End -Users, 2021 & 2031F |

| 9.4 India Sugar Market Opportunity Assessment, By Sources, 2021 & 2031F |

| 10 India Sugar Market - Competitive Landscape |

| 10.1 India Sugar Market Revenue Share, By Companies, 2024 |

| 10.2 India Sugar Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.