Vietnam Oil And Gas Pipeline Market (2025-2031) Outlook | Analysis, Value, Forecast, Industry, Companies, Trends, Revenue, Share, Size & Growth

Market Forecast By Location of Deployment (Onshore, Offshore), By Type (Crude Oil Pipeline, Gas Pipeline) And Competitive Landscape

| Product Code: ETC377310 | Publication Date: Aug 2022 | Updated Date: Apr 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 | |

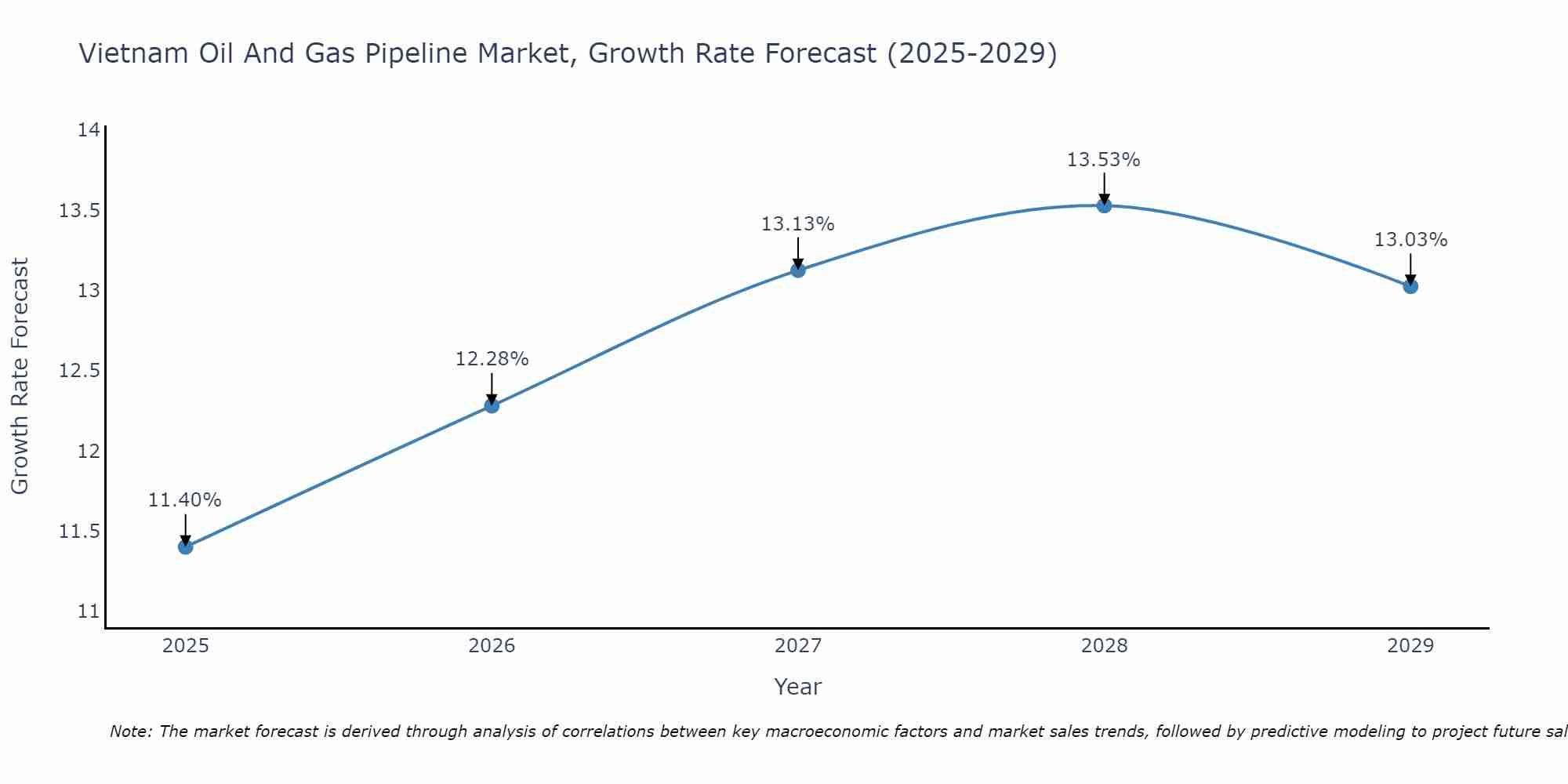

Vietnam Oil And Gas Pipeline Market Size Growth Rate

The Vietnam Oil And Gas Pipeline Market is projected to witness mixed growth rate patterns during 2025 to 2029. The growth rate begins at 11.40% in 2025, climbs to a high of 13.53% in 2028, and moderates to 13.03% by 2029.

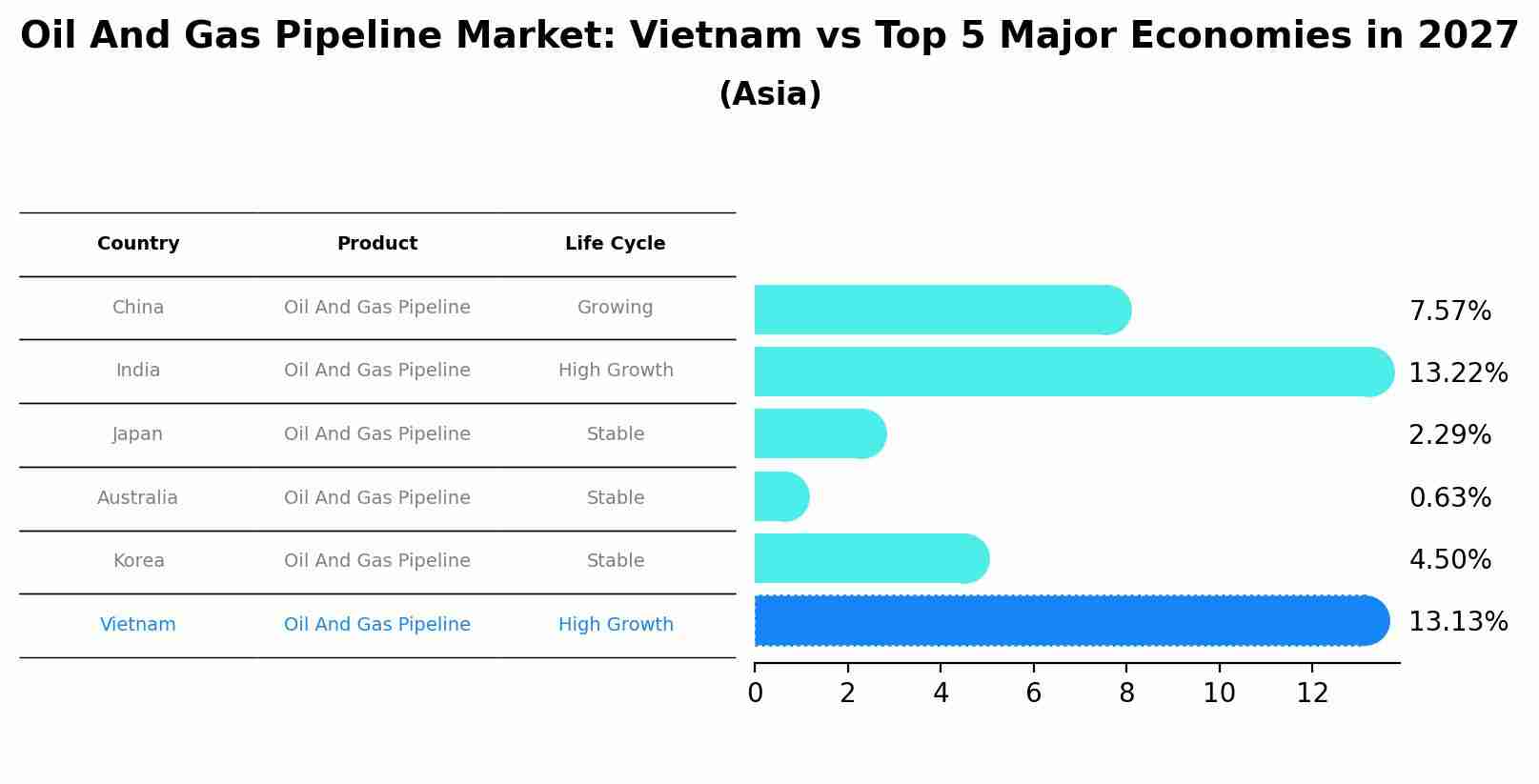

Oil And Gas Pipeline Market: Vietnam vs Top 5 Major Economies in 2027 (Asia)

Vietnam's Oil And Gas Pipeline market is anticipated to experience a high growth rate of 13.13% by 2027, reflecting trends observed in the largest economy China, followed by India, Japan, Australia and South Korea.

Vietnam Oil and Gas Pipeline Market Synopsis

The Vietnam oil and gas pipeline market are integral to the country`s energy sector. With increasing energy demand and exploration activities, the market has witnessed steady growth. Pipelines are essential for the transportation of crude oil and natural gas from production sites to processing facilities and distribution points. Safety, environmental compliance, and efficient transportation are key considerations in this market. Companies are investing in pipeline infrastructure to support the country`s energy needs and reduce reliance on imports.

Drivers of the Market

The Vietnam oil and gas pipeline market is primarily driven by the country`s growing energy demand and its efforts to enhance domestic oil and gas production. The government`s focus on expanding the exploration and production activities in offshore fields, as well as the development of new oil and gas infrastructure, such as pipelines, is a significant driver. Additionally, Vietnam strategic location as a transit hub for oil and gas shipments in Southeast Asia contributes to the market`s growth. The ongoing modernization and expansion of existing pipelines to ensure efficient transportation and minimize losses also play a pivotal role in boosting this market.

Challenges of the Market

The oil and gas pipeline market in Vietnam faces challenges associated with project delays, regulatory compliance, and environmental concerns. Building and maintaining oil and gas pipelines involves significant investments and complex regulatory approvals. Delays in project implementation can affect revenue projections. Additionally, addressing environmental concerns and ensuring pipeline safety are critical in the face of growing environmental awareness and stricter regulations.

COVID-19 Impact on the Market

The Vietnam oil and gas pipeline market faced disruptions during the COVID-19 pandemic as energy production and exploration projects were affected. Reduced demand for oil and gas, coupled with supply chain interruptions, impacted pipeline construction and maintenance. Companies in this sector faced financial constraints and had to reassess project timelines. The market`s recovery was closely tied to global oil and gas market dynamics and government policies to support the energy sector.

Key Players in the Market

In the Vietnam oil and gas pipeline market, a few key players have played pivotal roles in providing essential infrastructure for the country`s energy sector. PetroVietnam Gas Corporation (PV Gas), a subsidiary of the state-owned PetroVietnam Group, has been a major player in developing and operating the oil and gas pipeline network in Vietnam. PV Gas has made significant investments in building and expanding pipeline infrastructure to transport natural gas and petroleum products. Another significant player is Vietnam Oil and Gas Group (PetroVietnam), the state-owned oil and gas giant, which also plays a crucial role in the construction and operation of pipelines for oil and gas transportation. These leading players have not only focused on expanding pipeline capacity but have also contributed to safety and environmental standards in the Vietnam oil and gas pipeline market, supporting the nation`s energy needs.

Key Highlights of the Report:

- Vietnam Oil And Gas Pipeline Market Outlook

- Market Size of Vietnam Oil And Gas Pipeline Market, 2024

- Forecast of Vietnam Oil And Gas Pipeline Market, 2031

- Historical Data and Forecast of Vietnam Oil And Gas Pipeline Revenues & Volume for the Period 2021-2031

- Vietnam Oil And Gas Pipeline Market Trend Evolution

- Vietnam Oil And Gas Pipeline Market Drivers and Challenges

- Vietnam Oil And Gas Pipeline Price Trends

- Vietnam Oil And Gas Pipeline Porter's Five Forces

- Vietnam Oil And Gas Pipeline Industry Life Cycle

- Historical Data and Forecast of Vietnam Oil And Gas Pipeline Market Revenues & Volume By Location of Deployment for the Period 2021-2031

- Historical Data and Forecast of Vietnam Oil And Gas Pipeline Market Revenues & Volume By Onshore for the Period 2021-2031

- Historical Data and Forecast of Vietnam Oil And Gas Pipeline Market Revenues & Volume By Offshore for the Period 2021-2031

- Historical Data and Forecast of Vietnam Oil And Gas Pipeline Market Revenues & Volume By Type for the Period 2021-2031

- Historical Data and Forecast of Vietnam Oil And Gas Pipeline Market Revenues & Volume By Crude Oil Pipeline for the Period 2021-2031

- Historical Data and Forecast of Vietnam Oil And Gas Pipeline Market Revenues & Volume By Gas Pipeline for the Period 2021-2031

- Vietnam Oil And Gas Pipeline Import Export Trade Statistics

- Market Opportunity Assessment By Location of Deployment

- Market Opportunity Assessment By Type

- Vietnam Oil And Gas Pipeline Top Companies Market Share

- Vietnam Oil And Gas Pipeline Competitive Benchmarking By Technical and Operational Parameters

- Vietnam Oil And Gas Pipeline Company Profiles

- Vietnam Oil And Gas Pipeline Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Vietnam Oil And Gas Pipeline Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Vietnam Oil And Gas Pipeline Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Related Reports

- ASEAN Bearings Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Europe Flooring Market (2025-2031) | Outlook, Share, Industry, Trends, Forecast, Companies, Revenue, Size, Analysis, Growth & Value

- Saudi Arabia Manlift Market (2025-2031) | Outlook, Size, Growth, Trends, Companies, Industry, Revenue, Value, Share, Forecast & Analysis

- Uganda Excavator, Crane, and Wheel Loaders Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Rwanda Excavator, Crane, and Wheel Loaders Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Kenya Excavator, Crane, and Wheel Loaders Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Angola Excavator, Crane, and Wheel Loaders Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Israel Intelligent Transport System Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Uganda Precast and Aggregate Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Australia IT Asset Disposal Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

Smart Home Expo 2026

Industrial Facilities Management Expo 2025

4th Edition India Energy Conclave 2025

Media Expo 2025

Gas India Expo 2025

Our Clients

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero